Policy in Practice’s recommended changes to Universal Credit published in Work and Pension Committee report

Fabiana Macor Published on 05th November 2020

The Work and Pensions Committee has published the findings from its inquiry into Universal Credit and the wait for a first payment. In this blog post, Policy and Data Analyst Fabiana Macor, reviews the report and considers what changes are needed to Universal Credit and how the DWP and front-line organisations can target support around individual needs.

Policy in Practice’s evidence on financial resilience and the transition to Universal Credit

Policy in Practice gave evidence in-person and in writing to the inquiry. Our report, Financial resilience and the transition to Universal Credit, was supported by the Joseph Rowntree Foundation and published before the COVID-19 pandemic.

We recommended:

- The introduction of a targeted, non-repayable, grant to replace Universal Credit Advances for struggling households (at the time estimated to cost £2.7 billion over the managed migration period)

- A two-week run-on of Child Tax Credit, paid through the Universal Credit system

- Fortnightly payments of Universal Credit, starting with an initial payment at two weeks, based on the estimated monthly award amount

- Greater flexibility in processes such as recovery of overpayments and advances, claim verification and backdating, as called for by claimants, to help people to manage the transition to Universal Credit

We are pleased to see our recommendations taken forward in the Committee’s report, which opted for a non-targeted grant in place of our targeted recommendation, citing simplicity:

“In recommending a course of action, we have chosen an approach which offers simplicity: a simple amount of money, so it is clear to claimants what they can expect, and a simple process, which does not require the Department to carry out any additional means-testing or assessment of a household’s needs.”

In light of the COVID-19 pandemic and corresponding need for swift action, we agree with the Committee’s findings and recommendation for a non-targeted initial grant. However, targeted support will be key to successfully managing the consequences of the pandemic over the medium to longer term, when the matter of cost resurfaces, and to ensure that the most vulnerable are not left behind.

Evidence on links to financial hardship shows that changes to Universal Credit are needed

The Committee’s report began by stressing that the Department for Work and Pensions should consider seriously the evidence linking Universal Credit to financial hardship (such as food-bank use and rent arrears), regardless of whether existing research proves causality.

“Gareth Davies, the Comptroller and Auditor General , told us that the Trussell Trust’s work was “the best research we have seen on the link between UC first claims and use of food banks”

“DWP should more thoroughly consider the evidence linking Universal Credit to increased use of food banks, rent arrears and psychological distress and should use this in its overall strategy for protecting claimants’ safety and wellbeing.”

This has long been promised by the DWP. We support The Committee’s call for its publication and the view that existing research is a sure call to action. Our work with councils and other front-line organisations across Wales showed the association between Universal Credit debt to the council (rent and council tax arrears); known markers of increased hardship.

A seamless and flexible transition to Universal Credit is needed

Throughout the report DWP is urged to make claims to Universal Credit as seamless and flexible as possible, as well as providing truly holistic Universal Support. In addition, the report recommends that temporary increases to benefits, such as the £20/week increase to the Universal Credit Standard Allowance and Tax Credits, realignment of LHA rates to the cheapest third of local rents, are retained indefinitely and increased in future, in line with inflation.

The report cites the longstanding gap between benefit rates and living costs, which predates the onset of the pandemic earlier this year. Our recent blog post on who the most financially vulnerable residents in London are showed that these measures have helped an additional 6% of London’s pre-existing working-age low-income residents make ends meet. With a sluggish economy, there are also broader macro-economic benefits to consider from retaining emergency measures beyond 2021.

Better financial help is needed for people moving onto Universal Credit

The Committee adds that, for greater seamlessness, the DWP must reduce the five-week wait. This means eliminating it entirely for claimants moving to Universal Credit due to managed migration, who should continue to receive benefits such as Tax Credits which are not currently subject to a run-on payment. The fifth week of the waiting period can be slashed by implementing Faster Payments; a faster albeit more costly method of payment.

However, a seamless transition to Universal Credit cannot be achieved without some initial financial support during the wait, and more flexible Advance repayments centred around individual circumstances.

The Committee recommends that every first-time claimant should receive an initial ‘starter payment’ equivalent to 3 weeks of the Universal Credit standard allowance, with further support for people affected by the Special Rules for Terminal Illness, for example a higher starter payment or a simplified backdating process.

The report calls for advances to be renamed to make it clear they are loans. It also recommends that existing changes to the repayment of advances are brought forward to April 2021 rather than October 2021, and extended:

- Repayments set at 10% (current plans are to reduce to 25%) of the Universal Credit Standard Allowance

- Repayment cycle to be increased from 12 months to 24 months

Universal Credit payments should not be reduced by more than 30%

The idea of multi-dimensional, individualised support is not new but can be challenging to implement. Our 2019 report for the Joseph Rowntree Foundation highlights how data can be used to target support. We identified seven possible pressure points that could present obstacles to someone’s smooth transition to Universal Credit, which were cited in The Committee’s report:

- The level of existing debts and savings that a household has

- The likelihood of the first payment being delayed

- The household’s income after costs

- Whether the household will receive any run-on support

- The level of deductions from the household’s Universal Credit award

- For households moving from legacy benefits, whether their Universal Credit payments will be lower than what they received under legacy benefits

- Whether the household is ‘work ready’. 44% of people on Universal Credit are not expected to look for work because of illness or caring responsibilities (pre-pandemic figures)

Policy in Practice’s evidence identified 7 factors driving financial resilience that determine a household’s ability to cope with the transition to Universal Credit

In tandem with our findings above, The Committee asserts that the financial and mental health implications of repaying Advances should be understood multi-dimensionally:

“Advance repayments do not exist in a vacuum. Many people on Universal Credit face other deductions to their monthly payment; the Trussell Trust found that, as of May 2019, 440,000 (52%) of people repaying an Advance were also repaying other government debts”

Therefore, and noting that benefit payments are set at subsistence level, the Committee recommends the DWP to scrap exemptions to the maximum deduction from Universal Credit (which apply to sanctioned or in-arrears claimants); no claimant should have their Universal Credit payment reduced by more than 30% (a situation currently estimated to affect 20% of UC claimants).

It also proposes closer alignment with practices in the private sector which has had its regulatory framework shift in favour of customer focused collection practices, whereby the DWP:

- Seeks out alternative routes to tackle problematic cases

- Includes Universal Credit in the ‘Breathing Space’ initiative from the start, giving people in arrears a break from enforcement action

- Builds their approach to debt in line with guidance set by the private sector regulator, the Financial Conduct Authority

- Extends this to how it treats repayment of Tax Credit debt, which further reduces claimants Universal Credit payments. Specifically, repayments should amount to no more than 10% of the Universal Credit Standard Allowance and should be made only after Advances are repaid, with debts older than 6 years written off altogether.

Advances can serve a higher strategic purpose, too. They indicate that a claimant is struggling to cope with the transition to Universal Credit and, the report adds, should prompt the DWP to:

- Automatically accept request for payments to be made directly to landlord or housing providers

- Engage in personal budgeting support, including an evaluation of claimants’ financial situation and how future repayments will affect their financial resilience

Re-imagine debt: support centred around the person works

The Committee highlights that data relating to Advance payments can and should be used to identify vulnerable households and better support them, confirming our findings from the Cabinet Office’s Reimagine Debt pilot: households in debt to the council often faced multiple obstacles to their financial and emotional well-being. This makes them particularly responsive to targeted wrap-around support.

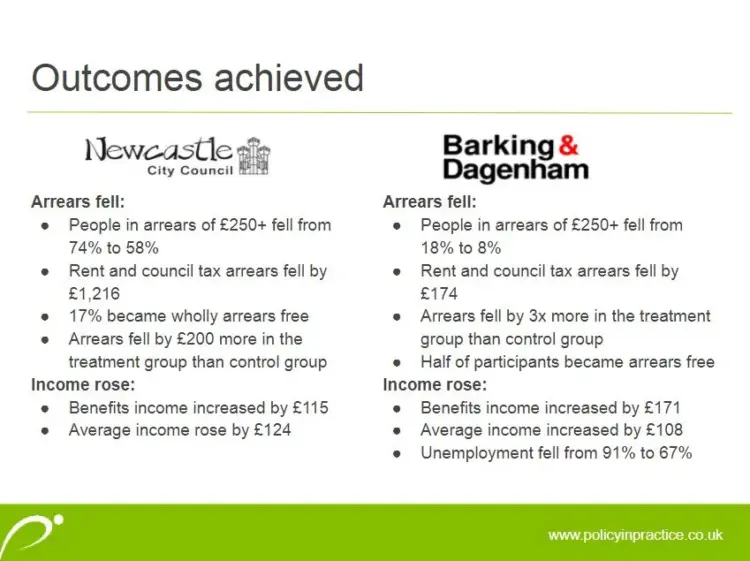

The pilot involved proactive approaches from Newcastle City Council and the London Borough of Barking and Dagenham to tackle debt and reduce arrears, after identifying eligible households with our Low Income Family Tracker plaform (LIFT).

LIFT confirmed the success of both councils’ new approach to tackling problem debt for the 18 and 10 households that were selected in Barking and Dagenham and Newcastle, respectively. Read more about the Re-imagine debt pilot and its evaluation.

Although both councils took different approaches to support, they shared the common view that support should be proactive and centred around the person. For the majority of cases in Newcastle, this involved a debt management plan, while in Barking and Dagenham this was done via the Community Solutions team. Our award-winning Better Off Calculator is already used by front-line organisations and advisers to help structure and guide these conversations.

Of the households LIFT tracked, the following outcomes were found:

The Cabinet Office backed Re-imagine Debt project saw arrears fall and incomes rise in Newcastle and Barking and Dagenham

Universal Credit stepped up to COVID-19, but more change is needed

As contributors to this inquiry we fully support the Committee’s recommendations contained within the report, particularly the recommendation of a non-repayable ‘starter payment’ and an individualised approach to support. We have previously called for nearly all of the recommendations, which are sensible. As the report says, there is now an urgent need for reform that has been highlighted by the increase in take up of Universal Credit under COVID-19.

In their nimble response to the economic fallout of COVID-19 the DWP has shown that the simplified and digital nature of Universal Credit can handle unprecedented demand. They have also shown their ability to adapt to changing circumstances and improve service delivery.

We support calls on the Department to continue to improve their service and address its weaker aspects. Universal Credit cannot stand still, it must continue to evolve to provide the backbone of the welfare safety net that our society needs and deserves.

Find out more

- Download Policy in Practice’s report Financial resilience and the transition to Universal Credit

- Download the Committee’s report Universal Credit: the wait for a first payment

Join our next webinars

- How to find the right debt solution for everyone on Wed 11 November. Register here

- 2020: Policy review of the year, and a forward look to 2021 on Wed 9 December. Register here

All our webinars are free and start at 10.30 for an hour and 15 mins. If you can’t make the date please register anyway to automatically receive the slides and recording. Contact hello@policyinpractice.co.uk with any questions.