What COVID-19 has taught us about the benefit system we want

Alex Clegg Published on 26th February 2021

The UK welfare system is complex, and people must understand a range of frequently changing benefits to know what support they are eligible for. The government has not had a consistent approach, despite Universal Credit’s initial aims to consolidate and simplify support, and it has not yet taken the opportunity offered by the coronavirus crisis to build a more coherent system. In this blog post we look at what Covid-19 has taught us about the benefit system we want.

The complexity has widened during the pandemic with the introduction of a number of new welfare measures and modifications to existing support. In the upcoming budget on Wednesday 3 March, we are likely to see significant changes to these measures, with many set to be rolled back despite the persistence of the pandemic.

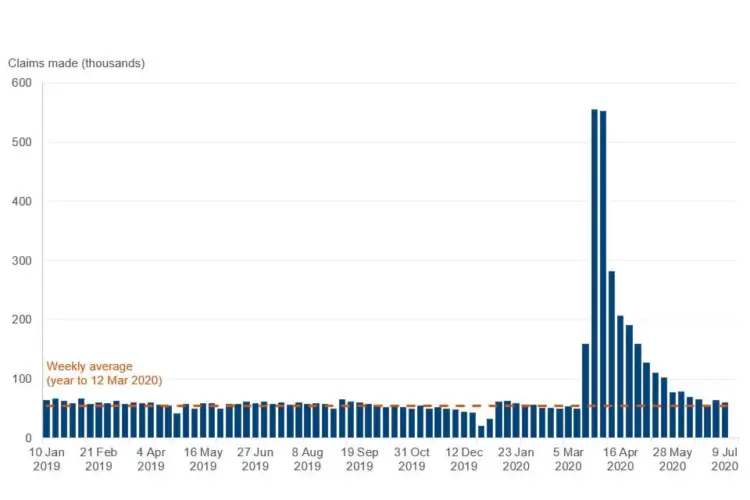

The number of people claiming Universal Credit soared from 3 million in March 2020 to 5.2 million in May and increased further to 6 million by January 2021. For many, this will have been their first experience of the complexity of the UK benefits system and the need placed on them to constantly adapt to shifting political and fiscal circumstances.

How the pandemic has impacted the UK welfare system

Before the start of the pandemic, the UK welfare system was at the tail end of a decade of austerity, shaped by falling real-term benefit rates, the extension of conditionality to in-work benefits recipients, and the introduction of austerity measures such as the benefit cap and the two child limit. This system was designed for a period of high employment and was focused on getting people back to work as quickly as possible.

The onset of the coronavirus crisis in March 2020 highlighted the weaknesses of this approach. In particular, the pandemic underlined the inability of standard welfare support to sustain households in the medium to long-term, as well as the inadequacy of statutory sick pay in the UK. The February 2021 report by the APPG on Health in All Policies on their inquiry into the 2016 Welfare Reform and Work Act finds that ten years of austerity and social security cuts had a profound effect on mental and physical health, even before the pandemic, and calls for a culture change from one that ‘dehumanises’ claimants to one that trusts and supports them. The December 2020 Marmot Review attributes the ‘high and unequal’ Covid-19 death toll in the UK partly to the effects of this austerity-driven poverty.

In addition to what COVID-19 has taught us about the benefit system these damning findings show that a complete rethink of the benefits system is needed post-pandemic, not a return to the status quo.

The government introduced a series of temporary measures in an attempt to mitigate the economic impact of the pandemic. These were the Coronavirus Job Retention Scheme (CJRS), the Self-Employment Income Support Scheme (SEISS), test and trace payments, the winter support grant, extra support for food banks, and a £20 per week uplift to the Universal Credit standard allowance. Despite inevitable teething problems, these measures were welcome and were, for the most part, introduced swiftly in reaction to the accelerating circumstances.

The DWP deserves praise for the speed with which it dealt with the substantial rise in Universal Credit claims, a situation that the Universal Credit system was able to manage capably, whereas the legacy benefit system, and indeed the benefits systems in the majority of European countries, could not. In addition, a more flexible approach was taken towards conditionality, as the previous strategy of getting people back to work as quickly as possible became increasingly less relevant as the employment crisis grew. This reduced the DWP’s administrative burden, allowing them to process claims much more quickly.

Universal Credit Claims: January 2019 – June 2020, DWP Universal Credit Statistics

However, the need for the array of emergency measures has served to highlight the existing gaps in the welfare safety net in the UK and the low levels of support previously available. Furthermore, boosting Universal Credit implied that those suffering due to the pandemic are more deserving of support than those suffering from chronic employment and personal crises pre-pandemic.

The many new types of support add to the complexity that must be navigated to fully understand provision. This is especially true for discretionary benefits administered by local authorities. These have been relied on to plug gaps in support throughout the pandemic yet, only 1 in 5 households that need a discretionary housing payment apply, suggesting that many families are unaware of the support available to them.

In addition, the amount of discretionary support available is often different based upon where people live. Policy in Practice research has found that the amount available through the Covid-19 Hardship Fund differs greatly between councils, as those with more generous council tax support schemes use up less of their funds covering existing council tax liabilities and therefore have more to spend on discretionary payments.

Moreover, local authorities, who already do so much with very stretched budgets, are relied upon to administer these discretionary payments. This puts a further strain on administrative resources. Policy in Practice works with many local authorities to help target discretionary support to those who need it through our Low Income Family Tracker (LIFT) platform, which uses household-level data to identify people who are struggling and who may be eligible for more support. These insights from the data analysis enable the local authority to target support directly.

The LIFT Dashboard helps councils to maximise the income of vulnerable households

Now, despite what COVID-19 has taught us about the benefit system we need, the persistence of the pandemic, and an economic and employment crisis that is likely to continue for some time, there are concerns that the government plans to roll back many of the measures brought in last year in the upcoming budget on Wednesday 3 March.

Four changes we can expect to see in Budget 2021

1. Removal of the £20 per week uplift to Universal Credit would mean a return to an inadequate level of benefit support

The most significant expected change is the removal of the £20 per week uplift to the Universal Credit standard allowance from April 2021. The government has come under sustained pressure to retain the uplift for at least another year but, as of now, has not stated that it will reverse its plans for removal. The government has talked-up the generosity of temporarily boosting Universal Credit by £20 per week, yet the uplift reversed cuts introduced by the benefits freeze from 2016. Its removal would represent a return to an inadequate level of benefit support.

Research by Policy in Practice in January found that if the uplift is removed, 683,000 households, including 824,000 children, would no longer be able to afford their essential needs. It would also be likely to damage the economic recovery, as providing economic support to low-income households is an effective way to boost consumer spending.

The chancellor has hinted at introducing a one-off payment to Universal Credit recipients of £500 or £1000 in order to make up for the removal of the uplift. Whilst this would mitigate some of the impact on current Universal Credit recipients, it would not help future claimants, of which there are likely to be a high number in the following year due to the continuing impact of Covid-19 on employment.

2. Local Housing Allowance will be refrozen, decoupling support from local rents

Local Housing Allowance will retain the increase it received in April 2020, but will be frozen at its current rate of the 30th percentile of local rents. Whilst this could mean the value of the LHA may increase in the short term if rents go down, it likely means that its value will fall below 30% of local rents in the long term. This freeze reintroduces the decoupling of support from local rents seen from 2016 to 2020, which housing charity Shelter has warned leaves low-income families unable to access even the cheapest local rents and pushes many people into debt or homelessness. The freeze is expected to decrease government spending on the LHA from £1 billion in 2020/21 to £300 million in 2025/26.

3. The announcement on the fourth Self-Employment Income Support Scheme (SEISS) is too late to allow self-employed workers to plan and budget

The Self-Employment Income Support Scheme allows self-employed people impacted by the coronavirus to apply for a grant. The chancellor is set to announce the SEISS covering February, March and April 2021 at the budget. This is unlikely to remain at the current 80% of profits and the announcement has been criticised for being too late to allow self-employed people to properly budget and plan. Martin Lewis, the founder of MoneySavingExpert, has said it is “unnecessarily cruel” to make people wait to know how much they will receive.

4. Reinstating the Minimum Income Floor will remove Universal Credit support for any self-employed workers whose earnings fall below the National Minimum Wage

The Minimum Income Floor (MIF) is calculated using the National Minimum Wage, multiplied by the number of hours a person is expected to look for and be available for work. If a person’s earnings from self-employment fall below this threshold, the government uses the Minimum Income Floor to calculate their entitlement to Universal Credit. It was suspended in April 2020 and is likely to be reinstated from April 2021.

For the many who started receiving Universal Credit at the beginning of the pandemic, their one year grace period before the MIF kicks in will have been used up by the time the MIF is reinstated. As the MIF is set at a level that is above the threshold for Universal Credit receipt, in practice this means that the majority of self-employed workers will receive no support from April.

The piecemeal approach to welfare does not help those in need

The piecemeal approach to welfare in the UK contradicts the stated aim of Universal Credit to simplify and consolidate benefits. The potential for Universal Credit to remove complexity by creating a genuine one-stop support system has been highlighted; doing so would help claimants to receive all the benefits they are eligible for.

Universal Credit was designed with a simplified mechanism of benefit allocation built-in which makes it puzzling why so many new measures of support are needed. Its high profile means it is much better known than other benefits that require a separate application process, such as Council Tax Support, which it risks obscuring.

The government’s piecemeal approach also means that people, and the organisations that support them, are forced to navigate a constantly changing benefits landscape and must frequently adapt to changes in support, often with little warning. The lack of clarity and advanced notice around upcoming changes to benefits, especially regarding the removal of the £20 Universal Credit uplift, whether or not there will be a one-off payment to make up for it, and the delayed announcement of the Self-Employment Income Support Scheme, serves as an example of this.

Will Quince, the Minister for Welfare Delivery, recently stated that the removal of the £20 uplift that the government “will continue to assess how best to support low-income families, which is why we will look at the economic and health context before making any decisions”, hinting that there may be further help packages to come. Whilst further support would be welcome, the lack of clarity around who will be eligible, how much it will be, and when it will be available only adds to the complexity of the system.

Vulnerable people will be unable to plan and budget if they don’t know what support will be available and this contributes to both economic and mental hardship during the pandemic. The uncertainty also impacts the decisions of legacy benefit recipients who are considering whether or not to move to Universal Credit. Many would be better off on Universal Credit with the £20 uplift but worse off without it, so the lack of clarity surrounding the removal of the uplift and any potential future measures leaves them unable to decide with confidence whether or not to switch.

Considering that changes such as the £20 uplift were brought in as an emergency response to the coronavirus crisis, there appears to be little rationale for removing them now. Rishi Sunak has cited the unaffordability of continued borrowing, yet there is a line of economic thinking that argues that the current historically low interest rates making government borrowing extremely cheap mean that now is not the time to focus on reducing the fiscal deficit. Instead, governments should spend to ensure the immediate protection of more vulnerable citizens and boost the economic recovery.

How the benefits system can be improved to provide a stronger safety net, throughout the pandemic and beyond

Strengthening the safety net provided by the welfare system throughout the pandemic and beyond requires widening the Universal Credit umbrella to include more benefits. This can be done using the mechanism to its full potential to create a genuinely one-stop system that would simplify the complex process of claiming, and ensure that people receive what they are eligible for.

It would also mean implementing a permanent financial uplift, ending the benefit cap and the two-child limit, and overhauling statutory sick pay. Making Universal Credit a genuinely one-stop, comprehensive benefit system would greatly simplify the complex benefits process and ensure that claimants receive what they are eligible for. The DWP’s response to the increase in claims during the pandemic shows that the administration would be able to deliver this.

In the meantime, there is a need for benefits advisors, support agencies and local authorities to be proactive in order to signpost people in need to appropriate support, ensuring that they are best supported by the benefit system we have right now, whilst we wait for the welfare safety net we all want to see.

Policy in Practice’s Low Income Family Tracker (LIFT) dashboards and Better Off Calculator have been designed to help simplify the complex benefits system and ensure that as people receive all the support they are eligible for. Use by many leading local authorities, LIFT uses household-level data to create insights that allow local authorities to identify their most vulnerable residents, monitor benefit take-up in order to target support, and track change over time.

Our Benefits and Budgeting Calculator, linked to from the GOV.UK website, allows people to input their personal circumstances to find out exactly what support they are entitled to, as well as giving information on how to apply. These tools are helping to simplify the complex benefits system and prevent vulnerable people from slipping through the gaps in the welfare safety net.

How councils are making a difference

Folkestone and Hythe District Council use LIFT to run targeted benefit take-up campaigns to boost the financial resilience of their residents. In the past year they have run campaigns focusing on take-up of pension credit, severe disability premiums, discretionary housing payments, as well as targeting support to self-employed people, and those most affected by Covid. Rotherham Council uses the Better Off Calculator to increase people’s income and employment opportunities. Find out more about their work here.

Next steps

Join our webinar on Wednesday 17 March where we share learnings from a powerful project, backed by the LGA and NHS Digital, to link data across adult services, children’s services, public health, the NHS, Police and Fire and Rescue Services. Find out more and register here.