How do the surplus earnings rules work in practice?

Zoe Charlesworth Published on 02nd July 2020

More than 2 million self-employed people have made claims for the Self-Employment Income Support Scheme (SEISS).

Many will receive a grant in June and July. These payments can be up to £7,500 and will be counted as earnings under Universal Credit. In August SEISS2 starts with payments of up to £6,750.

As a result, lots of self-employed households will be affected by the complex ‘surplus earnings’ rules for the first time. These rules are intended to spread high earnings in one month across multiple months, and will affect the amount of Universal Credit people receive. In this blog post we look at how frontline advisors can best support people in this situation.

Listen back to our webinar How to simplify the complexity of surplus earnings with Zoe Charlesworth and Duncan Hatfield from Policy in Practice, together with guest speaker Sue McCarron from Citizens Advice Wirral.

Advisors need a simple tool to make sense of surplus earnings rules

The Universal Credit surplus earnings regulations govern the treatment of spikes in income. These regulations are complex and require month-to-month calculations in order for advisors to help claimants. The treatment of “surplus earnings” is significantly more complicated than other Universal Credit regulations and the legacy benefit regulations that they were created to replace.

Advisors need an all-in-one simple tool to make these calculations and it’s particularly important to warn people of household income fluctuations in advance so they can set aside earnings to cover months when there will be no Universal Credit award.

A worked example to show how surplus earnings are calculated

Surplus earnings are calculated when earnings in an assessment period are more than the total of the surplus earnings threshold (£2,500) plus the level of earnings that would lead to a Nil UC award. This is called the Nil UC Threshold.

If a claimant receives income in an assessment period over the Nil UC threshold then the surplus earnings regulations will come into effect and some earnings will be carried over to the next Assessment Period.

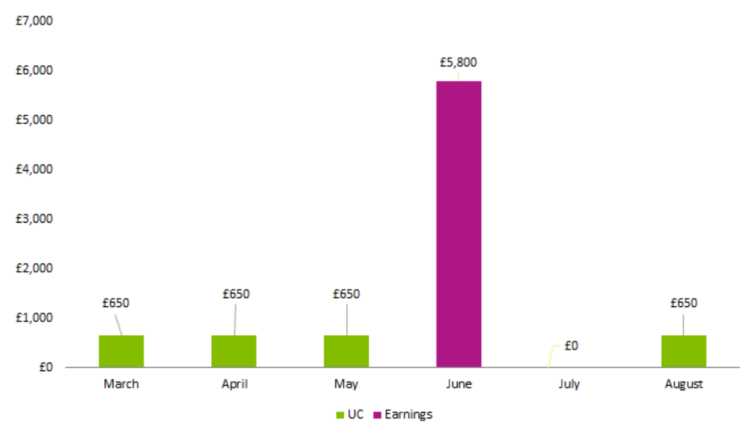

Mateo’s situation

Mateo is single and living in private rented accommodation. He is self-employed via a mobile cocktail bar. Since lockdown his income has fallen to £0. Mateo receives £650 Universal Credit per month. In June, he received a Self-employed Income Support Scheme payment (SEISS) of £7,500 (gross).

Calculation of Mateo’s surplus earnings

Month 1: Income of £5,800 is above the relevant threshold of £3,532 so Mateo’s UC is NIL

Calculate amount to c/f to month 2 (original surplus): £5800 – £3532 = £2,268

Month 2: Income used is £2,268 c/f from the previous month. His UC is NIL

Calculate amount to c/f to month 3 (adjusted surplus): £2,268 – £3532 = NIL

Month 3: Mateo receives full UC of £650

How Mateo’s household income fluctuates due to the surplus earnings rules

The impact of the surplus earnings and SEISS means that, from March to August, Mateo receives £8,400. Without the grant he would have received £3,900 (ie 6 payments of UC), so the grant is worth £4,500 (not £7,500 gross / £5,800 net)

This worked example of the surplus earnings rules and SEISS show that there are implications for advisors due to complexity and implications for the claimant in order to budget.

Little used before Coronavirus, how do surplus earnings regulations work in practice?

The Government responded to the economic fallout of COVID-19 by introducing the Coronavirus Job Retention Scheme (CJRS) and the Self Employed Income Support Scheme (SEISS). For self-employed Universal Credit claimants, SEISS is paid in 3-month blocks, leading to spikes in real-time income, which triggers the surplus earnings regulations.

For some furloughed employed earners, payment of wages only occurred once the employer received the government CJRS grant, again triggering surplus earnings provisions. As a result, many households will be affected by the complex surplus earnings rules for the first time.

For advisors, the triggering of the surplus earnings regulations means getting reacquainted with one of the most complex aspects of Universal Credit.

What fluctuating income means for claimants and for advisors

The claimant is expected to use their surplus income to live on until it is used up, at which point Universal Credit is reinstated. Claimants need to understand the impact of spikes in their income and, prior to May 2020, needed to re-apply for Universal Credit on a monthly basis if earnings fell in order to ensure their surplus is used up and that Universal Credit is reinstated at the earliest opportunity. From May 2020 the government has introduced temporary measures that will automatically re-assess eligibility to Universal Credit for up to 5 subsequent months and reinstate Universal Credit when applicable.

Advisors, meanwhile, need to understand the surplus earnings regulations and be able to convey complex explanations and calculations about the level of surplus, and its erosion over time, as simply as possible.

The threshold triggering surplus earnings has increased

In the initial Universal Credit regulations, the threshold at which surplus earnings were triggered was set at £300 per month above the amount of earnings that resulted in no UC. In other words, the surplus earnings regulations could come into play if earnings increased by more than £300 from one assessment period to the next.

However, it was recognised that this introduced an unnecessary level of complexity into a benefit system that was new to claimants. Plus, the low threshold meant that most claimants who were paid on a fortnightly or four weekly cycle would be caught by the surplus earnings provisions.

As a result, and as Universal Credit was rolled out, the threshold was increased to £2,500 per month. This increase was introduced on a temporary basis. In practice, the high threshold level meant that pre-COVID, the surplus earnings regulations very rarely came into play.

Why are surplus earnings treated differently?

The regulations were put in place to address concerns that claimants could manipulate the Universal Credit earnings assessment by colluding with employers and self-employed customers to pay in one large sum, covering many months’ work. Without the surplus earnings regulations, this would lead to no Universal Credit in one assessment period, but maximum Universal Credit in all other months. The surplus earnings regulations were therefore a means to ensure that any spike in income was taken into account for future months.

Fluctuating incomes make budgeting very hard

For households affected by the surplus earnings regulations, Universal Credit will not be awarded or will be reduced, until the surplus earnings are used up which can cause budgeting issues for those affected. In order to avoid falling into crisis, it’s critical that advisors help clients understand how much of a large one-off payment must be retained to cover living costs for future months when there will be no Universal Credit payment.

Advisors will need to help claimants to make sense of the surplus earnings regulations for the forseeable future, particularly given that there is a further block payment of SEISS is scheduled for August.

How to calculate the impact of surplus earnings in under 5 minutes

To help advisors give the best advice to clients facing surplus earnings we have added functionality to our award-winning Better Off Calculator that incorporates the impact of surplus earnings into an at-a-glance calendar of Universal Credit payments.

This makes it easy to see the combined impact of ongoing regular income, projected irregular earnings, and the surplus earnings provision, on a claimant’s Universal Credit award – all in one place. In addition, a message also gives information about the level at which earnings will trigger surplus earnings regulations.

Watch the short video by Duncan Hatfield, Policy and Operations Analyst, to see how the Better Off Calculator can be used to simplify the impact of surplus earnings.

Two recommendations for how the surplus earnings rules could work in the future

The re-emergence of the surplus earnings regulations in response to COVID-19 payments has provided a couple of useful indicators on how these regulations could work in the future:

- Prior to COVID-19 measures, a claimant would need to re-start the UC claim each month in order for surplus earnings to be used up or for UC to be awarded. This need for ongoing claimant action has temporarily been suspended and UC will automatically be awarded when applicable. This is a welcome amendment and this learning could usefully be carried forward post-Covid.

- The high surplus earnings threshold (£2,500) means that claimants are unlikely to be caught by surplus earnings due to weekly-based payment cycles. It also allows the claimant to retain greater amounts of earned income so allowing some of the surplus to be used to cover bills and debts. The £2,500 threshold should be retained to ensure that the regulations only come into play with higher income spikes.

Find out more about the Better Off Calculator

View details of our award-winning Better Off Calculator here or contact us for further details.