Tax credit cuts and the Living Wage: Do the numbers stack up?

Janet Harkin Published on 06th October 2015

In July’s Summer Budget, George Osborne announced two big cuts to work incentives in tax credits and the impacts of these changes are being discussed at the Conservative Party Conference this week.

The first cut to tax credits involves the taper rate which will increase from 41% to 48%. This means that tax credits are withdrawn more quickly when you earn more. The Treasury estimates that this measure will save £3.7 billion over the next five years.

The second involves the amount people in receipt of tax credits can earn before this withdrawal kicks in. This amount will fall from £6,420 to £3,850 per year for those receiving Working Tax Credit and from £16,105 to £12,125 per year for people only receiving Child Tax Credit. This measure, combined with reductions to the Universal Credit work allowances, is expected to save an additional £15.9 billion over the next five years.

These large savings for the Treasury will mean a substantial reduction in tax credits for households on low incomes. But the Government have argued that increases in the personal tax allowance and the National Living Wage, also announced in the Summer Budget, will compensate for the cuts, leaving households better off.

Yet, as Policy in Practice argued just after the Budget, the withdrawal of benefits and tax credits means that these policies will not benefit many low income families who will, in fact, see their incomes fall.

Why a Living Wage won’t compensate for tax credit cuts

Welfare is a complex system of work allowances and taper rates. When your earnings increase, your entitlement to benefits and tax credits decreases. This means that when people receiving benefits or tax credits get a pay rise, they don’t get to keep all of it – and sometimes they don’t get to keep any of it at all.

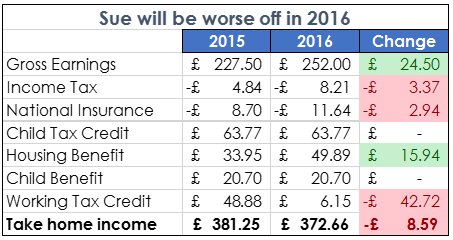

Let’s take the example of Sue who is a lone parent with one child who works full-time at the National Minimum Wage. In 2015, she has a weekly take home income of £381.25 per week.

In 2016, Sue will be worse off by £8.59 per week – around £447 per year. Her gross earnings will rise by £24.50 per week due to a higher wage and a higher personal tax allowance. But her Working Tax Credit will be reduced by much more, – £42.72 per week, due to this higher wage and the cuts to tax credits. Her Housing Benefit increases as a result of her lower tax credits (the benefit system is complicated), but not by enough.

What Sue gains from the Living Wage and a higher personal tax allowance does not compensate for what she’s lost in tax credits.

Analysing tax credit cuts on a local level

Policy in Practice has been working with local authorities to help them estimate and plan for upcoming changes to benefit and tax credits.

Analysing a cohort of low income households in receipt of Housing Benefit in one local authority, we found that all families in receipt of Working Tax Credit will have their tax credits reduced as a result of the higher withdrawal rate and lower income threshold. 33% will lose their entitlement to Working Tax Credit entirely.

On average, households receiving Working Tax Credit will lose an average of £44 per week – around £2,267 over the course of the year. By 2020, these same households will only see their earnings rise by an average of £36 per week as a result of a £9 National Living Wage and a personal tax allowance of £12,500.

Our analysis finds that the majority of families receiving Working Tax Credit (66%) will not see their earnings rise enough to compensate for the loss of tax credit income. Young parents under 25 in particular will lose out – 95% will be worse off – because they will not qualify for the National Living Wage.

Only 34% of people receiving Working Tax Credit will be better off. These households are more likely to be single people without children and owner-occupiers.

Other independent analysis has had similar findings. The IFS finds that only 13% of income losses due to benefit and tax credit changes will be offset by the National Living Wage. The Resolution Foundation argues that three million of the poorest working families will lose £1,350 each year.

The cumulative impact of the Summer Budget

Changes to tax credits are not the only welfare reforms coming to force in April 2016. Among other changes, the benefit cap will fall from £26,000 per year to £20,000 outside of London and £23,000 inside London.

Typically, the impact of each policy is analysed in aggregate, and in isolation. But because of the way policies interact, and have knock on effects, it is important to model these changes together.

Policy in Practice’s household-level analysis for local authorities can do just this. In one local authority, we found that the cumulative impact of the Summer Budget doubled the income reductions for low income households due to welfare reform, compared to what they had been to date.

On average, households have seen their incomes fall by £9.73 per week due to welfare reforms that have already been implemented (e.g. the under-occupation charge, benefit cap, etc.). This will rise to £18.44 per week as a result of the Summer Budget.