Natural migration: Policy in Practice’s evidence to the Work and Pensions Committee

Louise Murphy Published on 01st March 2019

This week, Zoe Charlesworth, Head of Policy at Policy in Practice, gave evidence to the Work and Pensions Select Committee on how moving onto Universal Credit will affect people and the differences between ‘natural’ and ‘managed’ migration.

The Committee’s questions follow the government’s announcement that the roll-out of managed migration will be delayed, and limited to a pilot of 10,000 claimants in 2019. As a result, around half a million more households will migrate ‘naturally’ onto Universal Credit, meaning their existing benefits claim will end and they’ll have to make a new claim for Universal Credit if they have a change in their circumstances. Unlike managed migration, households who naturally migrate onto Universal Credit are not given any transitional protection.

Zoe was joined on the panel by policy experts from the Resolution Foundation and the Institute for Fiscal Studies. This was followed by a panel discussion which heard about experiences from the frontline, with experts from Scope, Citizens Advice, the National Association of Welfare Rights Advisers and the Child Poverty Action Group all sharing evidence.

Click image to view Zoe Charlesworth, Policy in Practice, give evidence to the Work and Pensions Committee on Universal Credit: ‘natural’ migration

Key findings from our evidence

- 40% of households (around 200,000) who move onto Universal Credit without transitional protection will be worse off, by an average of £59.45 per week.

- 30% of households (around 150,000) who move onto Universal Credit without transitional protection will be better off, by an average of £44.30 per week. The other 30% will experience no change in income.

- Certain groups are particularly affected by natural migration onto Universal Credit: 72% of all low-income self-employed households and 90% of homeowners in receipt of tax credits will lose out. Additionally, people with savings over £16,000 were eligible for Tax Credits, but are not eligible for any Universal Credit.

- The way unearned income is treated under Universal Credit is different to how it’s treated under the legacy benefits system, and this results in significant changes to take home income for some groups.

“People should be able to check what impact a move to Universal Credit will have on their income before making life changing decisions.”

Zoe Charlesworth, Head of Policy, Policy in Practice

“People should be able to check what impact a move to Universal Credit will have on their income before making life changing decisions.”

Zoe Charlesworth, Head of Policy, Policy in Practice

People can use the free Benefit Calculator available at www.betteroffcalculator.co.uk, and organisations can email hello@policyinpractice.co.uk to request access.

Who gains and who loses when moving to Universal Credit without transitional protection?

1. Self-employed households lose

Self-employed households are likely to lose support when they move from legacy benefits to Universal Credit. This is because the minimum income floor, which assumes people are earning at least minimum wage, is applied under Universal Credit. 72% of all low-income self-employed household will lose out, losing on average £51 per month.

2. Households with savings lose

Households with over £16,000 also tend to lose out, because Universal Credit has a capital limit of £16,000. That means any household on Tax Credits with savings over £16,000 will lose their entire benefits award if they experience a change of circumstances which triggers natural migration. If they moved over through managed migration, they would be protected for one year.

In one of our case studies, someone with savings over £16,000 who increases their working hours from 15 to 20 hours per week will be worse off by £107.43 per month after the change in circumstances, and £549.04 per month worse off than it would be if it experienced the same change of circumstances under the legacy benefits system.

Even though Universal Credit tends to benefit working households and rewards those who increase their working hours, this is not the case if a household has savings over £16,000.

3. Disabled households and working lone parents lose

Other groups who lose out include disabled households; those in receipt of DLA or PIP see an average loss of £55 per week. Working lone parents will see an average loss of £8 per week.

4. Households that gain

The 150,000 (30%) of households that tend to gain through Universal Credit include employed households; they see an average gain of £9.13 per week. Households in receipt of ESA gain an average of £14 per week.

To read more about who gains and who loses support under Universal Credit, read our full report here.

How do changes to the way unearned income is treated in Universal Credit affect claimants’ income?

The detailed regulations about non-earned income differ between the legacy benefit system and Universal Credit. Specifically, there are differences in the types of unearned income that is taken into account and deducted from a benefits award, and which is disregarded when calculating benefits awards.

Three important types of unearned income that are treated differently under the legacy benefits system and Universal Credit are:

- spousal maintenance

- industrial injuries disablement benefit

- student grants for lone parents

These are all disregarded under the legacy benefits system yet taken into account under Universal Credit. This means that people in receipt of these types of income are likely to be worse off under Universal Credit.

We carried out case studies using our Better Off Calculator and found that:

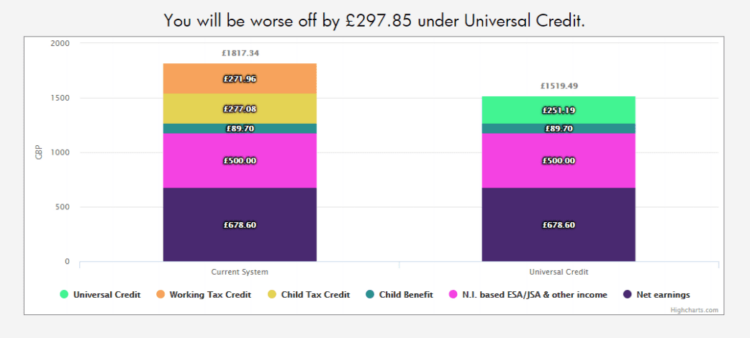

- A person working part time and in receipt of £450 monthly spousal maintenance would be £297.85 per month worse off under Universal Credit

- A person in receipt of Industrial Injuries Disablement Benefit who works part time and has 70% assessed level of disability would be £414.30 per month worse off under Universal Credit

- A student lone parent in receipt of a maintenance loan, childcare grant and parents’ learning allowance would be £277.08 per month worse off under Universal Credit

Case study: how take home income differs between the legacy benefits system and Universal Credit for someone in receipt of spousal maintenance

What sort of changes in circumstances trigger natural migration?

Natural migration is triggered when a household experiences a change in circumstances which means they would have previously had to make a new claim for any of the six legacy benefits which Universal Credit replaces.

As a result, the types of changes in circumstances that trigger natural migration vary considerably. They can range from moving house to a new local authority, becoming a full-time carer, having a child or becoming too ill to work.

Whilst claimants might expect big life changes, such as having a child, to affect their benefits claim, they are likely to be surprised by some of the changes that trigger natural migration. For example, lone parents claiming Income Support will naturally migrate when their youngest child reaches five, a seemingly insignificant change that is outside the control of the claimant.

It is vital that the DWP makes claimants aware of all of the changes in circumstances which will lead to natural migration onto Universal Credit, and informs them of how their income will change under Universal Credit.

Frontline organisations have also expressed concern that the changes of circumstances that trigger natural migration can often happen as a result of difficult personal changes, such as bereavement, separation, or becoming ill. This means that some households who lose income under Universal Credit will find natural migration particularly hard since this loss in income comes at an already tough time.

For example, a person who is unemployed and becomes disabled and ill, and therefore unable to work or prepare for work, will naturally migrate onto Universal Credit, and is likely to lose income.

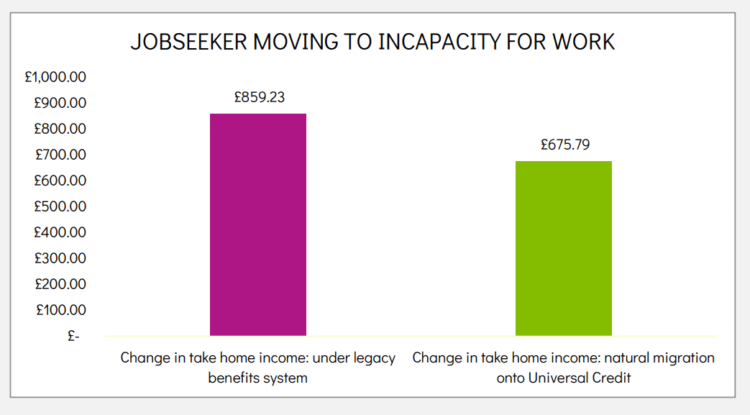

Some people maybe better off under Universal Credit after a change in circumstances, but not as better off as they would have been under the legacy benefit system. In one of our case studies, a job seeker who moves from claiming JSA to Universal Credit, and who is assessed for having Limited Capability for Work Related Activity and is in receipt of the standard daily living and mobility components of PIP, is better off after their change in circumstances, but is worse off by £183.44 per month under Universal Credit, compared to if they experienced the same change of circumstances under the legacy benefits system.

Case study: how take home income changes under the legacy benefits system and Universal Credit for someone moving from JSA to Universal Credit after becoming disabled and ill

Next steps

View Policy in Practice’s full Natural Migration evidence submission here.

Policy in Practice helps local authorities, housing associations and other frontline organisations to prepare people for migration onto Universal Credit. Read more about our Better Off Calculator here.

Zoe Charlesworth will be talking about how our Better Off Calculator helps people to understand how their incomes will change under Universal Credit in a webinar on Wednesday 15 May, find out more here.