What the close of the SDP Gateway means for disabled people moving to Universal Credit

Louise Murphy Published on 02nd February 2021

Wednesday 27 January 2021 saw the close of the SDP gateway. From now on, people receiving the Severe Disability Premium (SDP) in their legacy benefits are able to claim Universal Credit. If they experience a relevant change of circumstances, they will have to move from legacy benefits onto Universal Credit.

In any other year, the close of the SDP gateway would be a huge event due to the impact it will have on hundreds of thousands of people. But this is 2021: with ever-increasing numbers of people making new claims for Universal Credit, unemployment figures rising month on month, and the £20 a week uplift to Universal Credit at risk of being removed in the Spring, scrutinising the Universal Credit regulations may not be the top of everyone’s agenda at the moment. But whilst the close of the SDP gateway may not be making the headlines, it is worth pausing to reflect on the impact of this change and understanding which groups will be made worse off.

In this blog we look at the number of households that will be affected by the close of the SDP gateway and the change of circumstances that will trigger a move onto Universal Credit. We will then focus on the SDP transitional payments, and highlight some of the groups who will lose out if they move onto Universal Credit.

How many households will be affected by the close of the SDP Gateway?

As the name suggests, the severe disability premium is not a benefit in itself, but rather a premium that exists within other benefits. The severe disability premium can be added to Income Support, income-based Jobseeker’s Allowance (JSA), income-related Employment and Support Allowance (ESA) or Housing Benefit. (It can also be added to Pension Credit, but households over State Pension age are not affected by the end of the SDP gateway since they are not eligible for Universal Credit.)

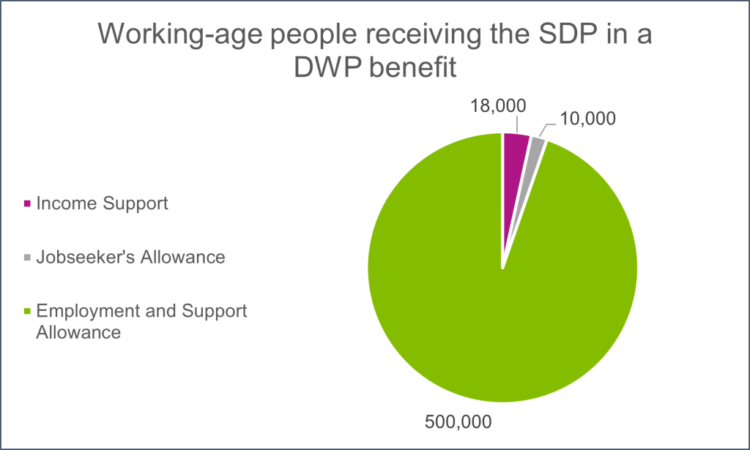

Over half a million households on Income Support, JSA or ESA get the Severe Disability Premium

According to government statistics, there were 528,000 working-age households in receipt of a SDP in their legacy benefits in 2017-18, the vast majority of whom (500,000; 95%) were receiving ESA.

95% of working-age people getting the Severe Disability Premium within a DWP benefit are receiving Employment and Support Allowance

This number is likely to have remained relatively stable since 2017-18 because working-age households claiming DWP benefits for the first time will have had to claim Universal Credit, even if they would have previously met the qualifying conditions for the severe disability premium. At the same time, the SDP gateway means that households in receipt of a SDP have, until now, been unable to move out of the legacy benefits system and onto Universal Credit. It is therefore reasonable to assume that the number of households in receipt of the SDP in their Income Support, JSA or ESA is around 528,000.

Hundreds of thousands of households on Housing Benefit get the Severe Disability Premium

Finding an accurate number of households in receipt of the SDP within their Housing Benefit is more difficult. Since Housing Benefit is administered by hundreds of councils across the UK, there is no central database holding this information. To get an idea of the proportion of households on Housing Benefit who are in receipt of the SDP, we have analysed Policy in Practice data provided by 24 councils across England and Wales in 2020-21. We found that 24% of working-age households claiming Housing Benefit in these councils (185,000 households) were in receipt of the severe disability premium.

Change of circumstances that can trigger a move onto Universal Credit

The end of the SDP gateway means that households currently receiving the SDP can, for the first time, make a claim for Universal Credit – but they won’t be forced to do so unless they experience a relevant change of circumstances. Moving onto Universal Credit due to a change of circumstances is called natural migration.

Some of the changes of circumstances are life events that people may expect to impact their benefits, such as

- Moving into, or out of, employment

- Becoming responsible for a child

- Moving home to a new local authority

Importantly, many of these life changes that trigger a move onto Universal Credit have been happening much more frequently in 2020 and 2021 than in previous years due to the impact of COVID-19.

Many of these natural migration triggers relate to changes in employment status. If you are receiving legacy benefits and start a full-time job, are made redundant, move out of employment due to illness or change your working hours above or below the Working Tax Credit threshold, you will move onto Universal Credit.

Working households who are in receipt of the SDP are especially likely to have experienced changes due to COVID-19. Recent Citizens Advice research found that disabled people were almost twice as likely to be facing redundancy than the general public. Whilst 17% of the overall population faced redundancy, this rose to 27% for disabled people and 37% of those who said their disability has a large impact on their day-to-day life.

Some of the other changes that trigger a move onto Universal Credit are perhaps less obvious. For example, a lone parent in receipt of Income Support will be forced to make a new claim for Universal Credit as soon as their child turns five. For more detailed research on natural migration to Universal Credit, see our 2019 evidence submission to the Work and Pensions Committee.

Severe disability premium: transitional payments

To make up for the loss of the severe disability premium when people move onto Universal Credit, the government introduced SDP transitional payments. These will be included in the Universal Credit award as a transitional element. These payments only compensate for the loss of a SDP, and are only available to people who have received a SDP within their Income Support, JSA or ESA in the month before they claim Universal Credit and continue to meet the eligibility conditions for SDP. They are not available to people who are only receiving a SDP within their Housing Benefit or to people claiming benefits for the first time.

There are three different levels of transitional payments:

- £405 a month where joint claimants were receiving the higher couple rate SDP in their legacy benefits. The higher couple rate SDP is paid when both members of the couple are eligible for SDP.

- £285 a month for single claimants not in the Universal Credit limited capability for work-related activity (LCWRA) group. This is a direct replacement for the £65.85 a week SDP. This amount is also paid to couples where only one member is eligible for SDP and they are not receiving the LCWRA component in Universal Credit.

- £120 a month for single claimants who have been determined as having LCWRA. These claimants receive a lower amount of transitional protection because they will be receiving the LCWRA element of Universal Credit. This amount is also paid to couples where only one member is eligible for SDP and they are receiving the LCWRA component in Universal Credit.

Three groups who lose out if they move to Universal Credit, despite transitional payments

1. Households receiving the SDP in their Housing Benefit only

Households who are receiving the SDP in their Housing Benefit only do not qualify for transitional payments. These payments are only available to people who were receiving the SDP in their JSA, ESA or Income Support. This means that people who are disabled and in work, who are currently receiving Housing Benefit and working tax credit, will lose out if they have to claim Universal Credit. This is especially concerning in the current economic climate when working disabled people are often facing redundancy or cuts to their working hours.

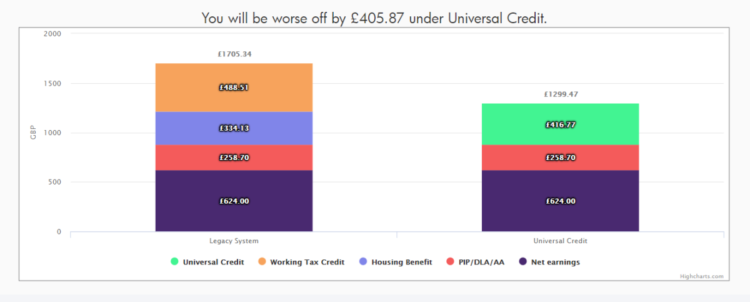

Case study: Paula’s story

Paula is disabled and receives Personal Independence Payment (PIP), the daily living part at the standard rate. She lives alone, so she qualifies for the SDP in her Housing Benefit. She works 16 hours a week and receives working tax credit to top up her earnings.

Paula moves house to a new local authority and so she must make a new claim for Universal Credit. Despite having received the SDP within her housing benefit, she is not eligible for the SDP transitional element in her Universal Credit. When Paula claims Universal Credit, she is £406 a month worse off.

If Paula moves house triggering a move to Universal Credit she will be £406 a month worse off

2. Households who lose other elements of their legacy benefits when they move to Universal Credit

The transitional element of Universal Credit only compensates for the loss of SDP. This means that people can still lose hundreds of pounds a month when they move to Universal Credit depending on their circumstances. Indeed, disabled people in receipt of the Enhanced Disability Premium (EDP) have never benefited from the SDP gateway and have already been moving onto Universal Credit. They tend to receive less money under Universal Credit since there is no equivalent for the EDP within Universal Credit, and they do not receive any transitional payments.

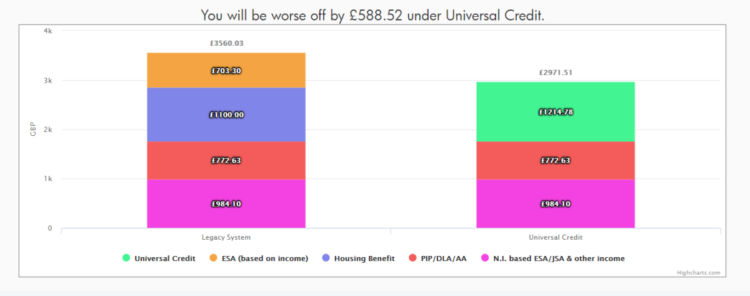

Case study: Sam and Peter’s story

Sam and Peter move to Universal Credit due to a change of circumstances. They used to receive the SDP in their ESA and Housing Benefit. They are both disabled and care for each other, and are both assessed as having Limited Capability for Work-Related Activity (LCWRA). They have both previously worked and paid national insurance, so they qualify for New-Style ESA. They have an underlying entitlement to Carers Allowance and receive the carer element of Universal Credit.

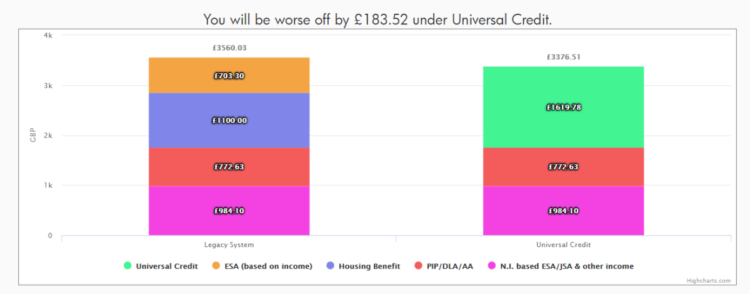

Without the SDP transitional payment, they would be £589 a month worse off when they move to Universal Credit. However, even when they receive the transitional element of £405 a month, they are still £184 a month worse off under Universal Credit than under the legacy benefits system. This is because they are not compensated for the loss of their enhanced disability premium. If the £20 a week uplift to Universal Credit is dropped in April, people like Sam and Peter will be even worse off if they have to claim Universal Credit.

Without the SDP transitional payment, if Sam and Peter moved onto Universal Credit they would be £589 a month worse off

If Sam and Peter moved onto Universal Credit they would still be £184 a month worse off even with the SDP transitional payment

3. Households whose transitional payments will erode quickly

The SDP transitional element is a measure introduced by the government to soften the blow when people move from legacy benefits onto Universal Credit. It is designed to decrease over time, so that in the long run, no one will be receiving SDP in working-age legacy benefits or a SDP transitional element. If your circumstances change and any element of your Universal Credit (apart from the childcare costs element) increases, your transitional element will decrease by the same amount. For some households, this erosion will happen quickly.

Case study: Kate’s story

Kate is a single parent who has a child in January 2021, prompting a move from legacy benefits to Universal Credit. She was receiving the SDP in her ESA and qualifies for the LCWRA element of Universal Credit. Her transitional element is £120 a month.

In April, her rent will increase by £50 a month. Her housing costs element increases to reflect this. But at the same time, her transitional element is decreased by £50 a month (to £70 a month) meaning the overall amount of Universal Credit she receives stays the same.

If Kate has another child next year she’ll receive an additional amount in her child element of Universal Credit (in 2020-21 this is £236). As before, this increase will be offset by a reduction to her transitional element. Because the £236 increase is greater than her £70 transitional element, her transitional element is reduced to zero.

The value of Kate’s transitional protection could decrease to zero over a short time

In the course of 18 months, by experiencing some common life changes, Kate no longer benefits from the SDP transitional payments. As a result, when she faces additional expenses such as higher rent or the arrival of a new baby, Kate’s benefits will not increase like they would have done if she were still to receive legacy benefits. In the context of COVID-19, when people like Kate are more likely to be facing redundancy and eviction, these types of changes are not uncommon.

Covid-19 accelerated the natural migration to Universal Credit which means that many disabled people miss out on transitional protection

It has been known since Universal Credit was first launched that many thousands of disabled people will lose out when they move onto Universal Credit. This was an intentional policy decision; ministers chose not to include disability premiums when designing Universal Credit. Yet the scale of the problem is bigger than was perhaps imagined back in the 2010s. More and more people are experiencing natural migration onto Universal Credit due to changes in their circumstances, especially in light of COVID-19. This means that more people will miss out on full transitional protection.

Managed migration (or ‘Move to UC’) was, until recently, forecast to be finished by the end of 2023. It has now been pushed back, and the small-scale pilot in Harrogate is now on hold. In 2018, the OBR predicted that 300,000 people would move to Universal Credit under managed migration in 2020-21 and 1.1 million in 2021-22. In reality, only 80 households have been involved in the Harrogate pilot so far.

This means that many households who would have been part of ‘Move to UC’ and received full transitional protection will no longer do so. Whilst some disabled households will receive SDP transitional payments, these only compensate for the loss of a severe disability premium, whereas full transitional protection compensates for all other losses like the enhanced disability premium. As we saw in the case study of Sam and Peter, this difference can be worth hundreds of pounds. Under ‘Move to UC’, Sam and Peter’s transitional protection payments would be £589, whereas their SDP transitional element is £405, a reduction of £184.

Close of the SDP gateway: a personal benefits calculation is essential before moving onto Universal Credit

Welfare rights advisors in local authorities, housing associations, local Citizens Advice and other charities have an increasingly difficult task to do. Whilst the Secretary of State for Work and Pensions is encouraging people to move to Universal Credit to benefit from the £20 a week uplift and celebrating the close of the SDP gateway, in reality the picture is much more complex.

There will be some people who will be slightly better off whilst the £20 a week uplift is in place, but worse off if it is removed. Others will be much worse off under Universal Credit, like Paula and Sam and Peter above. And finally, for many people currently in receipt of the severe disability premium, the transitional element will protect from any financial losses in the short term, but when their rent increases in April, or they have another child, their transitional element will get eroded away.

As DWP Minister, Will Quince, advised, anyone looking to move from legacy benefits to Universal Credit is encouraged to check their eligibility before doing so. Policy in Practice’s free Better Off Calculator is listed on GOV.UK and can be accessed here. This advice is particularly prudent now, given the close of the SDP gateway.

https://twitter.com/policy_practice/status/1351255824480542722?s=20

Find out more

- Our Better Off Calculator allows advisors to compare someone’s entitlement under legacy benefits to Universal Credit, and our scenario feature allows you to understand the impact that a change of circumstances will have on someone’s benefits award. You can access the free version of the calculator here, or you can find out more about the advisor version here.

- If you are considering switching from legacy benefits to Universal Credit, we encourage you to seek advice from Citizens Advice or another welfare rights organisation.