Three ways DWP can improve young people’s access to work

Louise Murphy Published on 28th September 2020

Young people are typically one of the groups most heavily impacted by recessions and new labour market statistics show that the recovery from Covid-19 will be no different. The number of young people in employment is falling at its fastest rate since 2009. In this blog post we look at what the numbers reveal about young people’s access to work, and what can be done to improve this.

Policy in Practice gave evidence on young people’s access to work

Earlier this year Policy in Practice submitted evidence to the Work and Pensions Committee’s call for evidence into the Department for Work and Pension’s preparations for changes in the world of work. Part of our submission focused on areas where the benefits system doesn’t work for young people, including students and apprentices. The problems we highlighted are even more pressing in light of Covid-19 as more young people need support to get into employment.

Young people have been hit hard by Covid-19

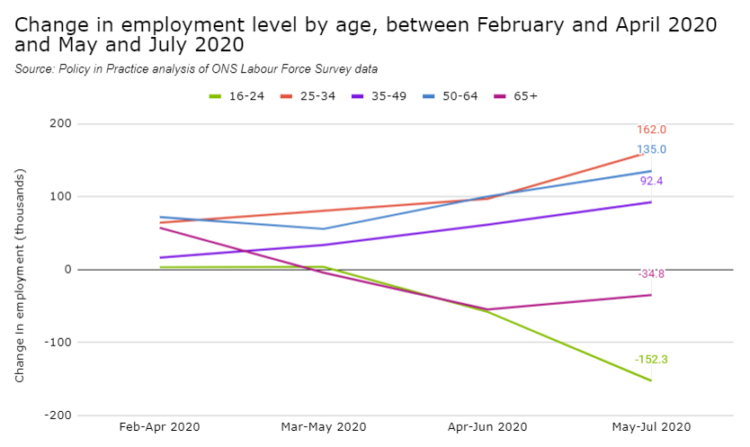

Young people have been especially hard hit by Covid-19. Recent released ONS Recent Labour Market Survey data shows that, despite a positive picture overall, employment rates for young people fell significantly between February and July 2020. Between May and July 2020, the number of 16-24 year olds in employment decreased by 152,300. This decrease was much larger than for any other age group.

During Covid-19 employment rates for young people have fallen more than any other age group

In recent months, the government has announced its ‘Plan for Jobs’ to help young people recover from the impact of Covid-19. These plans include:

- The Kickstart Scheme. This will create new, fully subsidised jobs for young people aged 16-24 who are claiming Universal Credit and at risk of long-term unemployment. Government funding will cover six-month job placements, paying the National Minimum Wage for 25 hours a week.

- Cash incentives to encourage businesses to take on new apprentices. Employers are being offered £2,000 for each new apprentice they hire aged under 25, and £1,500 for each new apprentice aged 25 and over.

- Doubling the number of DWP work coaches to 27,000.

Three actions DWP can take to improve young people’s access to work

In the context of Covid-19 and these high levels of youth unemployment, the DWP can do more to ensure that young people are supported during Covid-19, and have the skills they need to get into and progress in work.

1. Young people should receive more income from Universal Credit

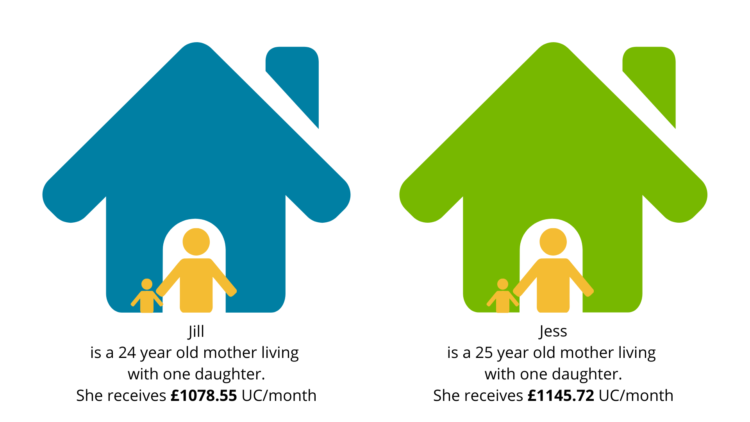

Young people receive less income from Universal Credit than older people, even if their circumstances are otherwise identical. This is because Universal Credit standard allowances are lower for people aged under 25 than for people 25 or over. Single people aged under 25 receive £67.17 per month less than those 25 or over, and couples receive £105.45 per month less.

Jill receives £67.17 a month less to support her family than Jess because she is a year younger.

In addition, most people under 18 do not qualify for Universal Credit at all. There are exceptions, for example for those who are responsible for a child or have limited capability for work. However, for the majority of 16-17 year olds who have lost work due to Covid-19, there is no safety net available to them if they cannot fall back on parental support. Importantly, this also means that many 16-17 years olds will miss out on support from the Kickstart scheme, since claiming Universal Credit is one of its eligibility criteria.

2. Universal Credit eligibility should be extended to full-time students

Universal Credit is available for full-time students in further education if they are the primary carer for a child, have a partner who is eligible for Universal Credit, or are disabled and have limited capability for work. However, young people who do not fall into any of these groups are not eligible for any Universal Credit.

This creates a significant barrier to further study for many young people, and limits their access to a number of employment sectors and vocations that require higher education. It has also left many students who were previously able to make ends meet by working part-time without a lifeline if they lost their job due to Covid-19.

In addition, students who do qualify for Universal Credit are often left with little support due to the way that student loans and grants are taken into account. Some loans and grants, for example those intended to cover books, equipment or childcare costs, are disregarded in full during Universal Credit calculations.

However, student maintenance loans, the main source of student income for the majority of students, are treated as income. Indeed, it is the maximum amount of student loan available to you that is used in the UC calculation, even if this is not what the claimant actually receives.

This has a big impact on students who are not receiving parental support: their UC calculation will often include a parental contribution to their student loan, even though in reality this income is not being paid. This means that some students will be left with no income from their parents, low income from student finance, and low income from Universal Credit.

In short, young people without financial support from their parents or partner (who do not have significant savings themselves) are left without a safety net.

We recommend that Universal Credit eligibility is extended to those in further education. Doing so could help to empower claimants to make the right decisions for their long-term career prospects. This is especially important in the context of Covid-19, where youth unemployment is expected to rise and remain high for the foreseeable future.

Supporting young people into further education and training could help to develop skills for the workplace while the labour market provides few opportunities in the coming years.

3. DWP should remove financial barriers to taking up apprenticeships

The government has announced support to encourage businesses to take on new apprentices. However, more needs to be done to make apprenticeships a financially viable option for young people in low-income households.

Households in receipt of means-tested benefits such as Universal Credit are financially penalised when a young person chooses to take up an apprenticeship. This is because young apprentices are not treated as children, so their parent or guardian is not eligible for child benefit, the child element of Universal Credit, or the Universal Credit Work Allowance. If the apprentice is over 21, their parent or guardian will also have a non-dependant deduction applied to their Universal Credit.

In comparison, parents or guardians of young people who are in non-advanced education or training are eligible for child benefit, the child element of Universal Credit and the Universal Credit Work Allowance.

In many cases, the combination of the loss of benefits and the low minimum wage for apprentices which is just £4.15 per hour for apprentices under 19 and for all apprentices in their first year, means it is not financially viable for a young person to start an apprenticeship.

Case study: why apprenticeships should be paid minimum wage

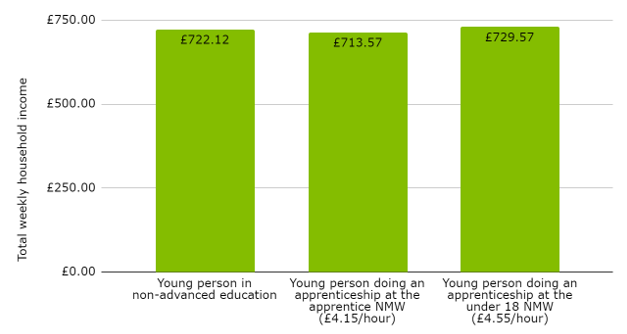

A young person is living with their parent who is earning £507 per week, receiving £194.07 per week Universal Credit and £21.05 per week Child Benefit. Their total weekly household income drops by £8.55 per week when they move from non-advanced education into an apprenticeship. However, if apprenticeships were paid at the minimum wage, household income would increase slightly by £7.45 per week.

This case study illustrates the difference in a young person’s income when they are paid at the apprenticeship national minimum wage (middle column) compared to the age-related national minimum wage (right-hand column). Apprenticeships would be more financially feasible if paid at the age-related minimum wage.

This impact is even more pronounced for disabled young people. If a disabled young person was to take up an apprenticeship, their parent or guardian would no longer be eligible for the disabled child element of Universal Credit, as well as the other elements mentioned above. This, combined with the higher costs of work that disabled people face, means it is often financially impossible for disabled young people to take up apprenticeships.

Given that Citizens Advice recently found that disabled people were more likely to face redundancy as a result of Covid-19 than the rest of the working population, more needs to be done to ensure that disabled people can get the skills they need to find employment.

We recommend that apprentices should be paid their age-related national minimum wage. This would reduce the burden on low-income households and make apprenticeships financially feasible for these households.

We also recommend that parents and guardians of young people doing apprenticeships should be eligible for or child benefit, the child element of Universal Credit and the Universal Credit Work Allowance.

Finally, we also recommend that additional support is given to disabled young people to make sure that apprenticeships are a viable option for them.

How DWP can act to better support young people’s access to work

We recommend that the DWP does more to support young people who are struggling as a result of Covid-19:

- Universal Credit standard allowances for people under 25 should be raised to be in line with people aged 25 and over.

- Universal Credit eligibility should be extended to full-time students.

- Apprentices should be paid their age-related national minimum wage.

- Parents and guardians of young people doing apprenticeships should be eligible for child benefit, the child element of Universal Credit and the Universal Credit Work Allowance.

Find out more

- Read Policy in Practice’s submission: DWP’s preparations for changes in the world of work

- Policy in Practice helps local authorities, housing associations and other frontline organisations to help people understand how the welfare system can help them move into employment. Read more about our Better Off Calculator here

Join our next webinars

- How to predict next year’s demand for your customer-facing services now on Wed 7 October. Register here

- How to find the right debt solution for everyone on Wed 11 November. Register here

- 2020: Policy review of the year, and a forward look to 2021 on Wed 9 December. Register here

All our webinars are free and start at 10.30 for an hour and 15 mins. If you can’t make the date please register anyway to automatically receive the slides and recording. Contact hello@policyinpractice.co.uk with any questions.