Evidence: How well has DWP responded to the Coronavirus pandemic?

Deven Ghelani Published on 30th April 2020

Policy in Practice’s response to a survey about how DWP responded to the Coronavirus pandemic has been published by the Work and Pensions Committee. In our submission, summarised in this blog post, we shared highlights from our work supporting thousands of claimants from late March to early April 2020.

Read Policy in Practice’s submission to Work and Pensions Committee inquiry into DWP’s response to the Coronavirus pandemic

Our submission was based on three main sources:

- Analysis of the impact of government measures to help households hit by Coronavirus (COVID-19) available here

- A systematic and personalised response to 1,209 people whose incomes have been affected by Coronavirus, and the measures put in place to contain it, available here

- Content from a Policy in Practice webinar attended by over 800 frontline organisations summarising the content below in an interactive video presentation with slides, available here

If your income has been affected by Coronavirus, you can find out the support available to you here, and you check your eligibility for Universal Credit and other support using our free calculator.

DWP responded to the Coronavirus pandemic well but some gaps remain

We believe that the welfare and employment measures that were rapidly put in place by the government were necessary. The measures make it more likely that people will take the required steps to help control the virus knowing they are more likely to stay in work, be able to meet their financial commitments, and be supported financially.

The pace of implementation, from policymakers and those delivering operationally across central government, local government, and the private and voluntary sector, has been genuinely impressive. However, such speed of deployment undoubtedly means there will be gaps in provision. In pointing these out, our aim is to offer constructive ways to plug these gaps, rather than to be critical of the measures, which we welcome.

Our findings are echoed by others, as the Committee found. Rt Hon Stephen Timms MP, Chair of the Work and Pensions Committee, said:

“Hearing from people with first-hand experience of the benefits system is a crucial part of our scrutiny of the DWP. It’s clear from what we’ve heard that DWP staff are working very hard and have made great strides in adapting to the unprecedented strain on the benefits system.

“But we’ve also heard from people who are still facing serious difficulties. Disabled people have been particularly hard hit: their living costs have gone up, but their benefits have stayed the same. And there’s an urgent need for more clarity for people who are self-employed. We hope that Ministers will look carefully at what people have told us, and make changes.

Response to questions in the call for evidence

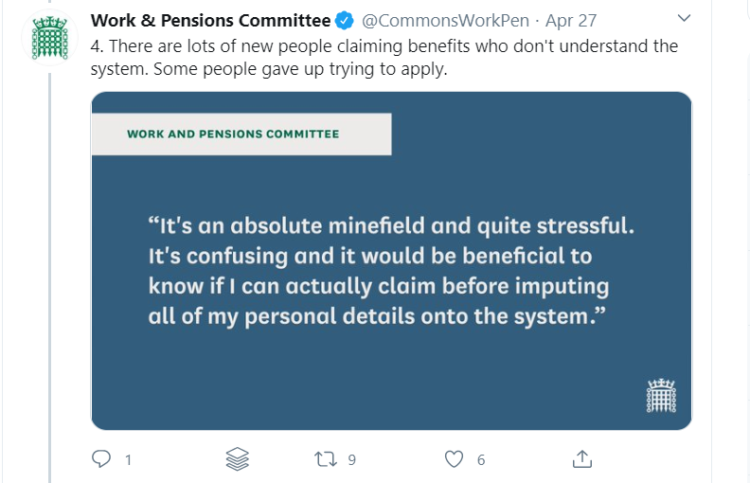

- Policy in Practice is seeing many more enquiries from people who are coming into contact with the benefit system for the first time. Conversations with our clients and partners indicate a ratio of three new claimants for one existing claimant.

- The general picture of new claimants is that those waiting to be paid through the furlough/self-employed scheme who are struggling financially are hesitant to claim benefits for various reasons (e.g. thinking they won’t qualify for Universal Credit if they get paid through the furlough scheme, or worried that they’ll have to repay their Universal Credit). We encourage them to claim. People who haven’t used our calculator before posting aren’t sure how much to expect, and have typically thought that they would receive more support. For those coming into contact with the benefits system for the first time, there is concern that the amount available will not cover their basic bills.

- The general view from existing claimants is confusion over planned increases and whether they will be eligible to receive them. For example, people on Working Tax Credits are concerned that they haven’t yet seen the increase – we explain that it will most likely apply as it is paid in arrears. Similarly, people on JSA/ESA/IS are confused about why it won’t apply to them. There is also a level of confusion amongst those already in receipt of tax credits about whether they should move to Universal Credit or not. For some, this would be advised but others should remain in receipt of tax credits. This decision requires personalised advice.

- We have advised those making a claim for Universal Credit to be patient, and have heard that claims are processed relatively quickly once completed. However, there remains confusion about whether the claimant should contact DWP or wait for a call, as well as how requested paper evidence should be submitted. This appears to result from online advice from the DWP not matching the current circumstances. Generally, we find it helpful to be able to point people to one department, as opposed to three under the legacy system, although we think that council tax support, free school meals and other support available locally should be much better signposted. Councils have seen a significant increase in new claims (2x – 4x) but not to the same extent as DWP.

- The introduction of responsive measures by the departments to claimants’ key concerns is promising. Examples of responsive measures include the extension to the furlough scheme, improvements to verification i.e. enabling the government gateway as an ID check for self-employed people, the ‘we’ll call you service’, flexibility around deadlines for evidence submission, and the extension of the time for which working hour changes can be ignored for tax credits.

- We have had many queries from those that have slipped through the net, the main categories are:

- Employers not willing to put employees on furlough, or not paying furloughed workers wages until reimbursement arrives. We encourage them to apply for UC if eligible and encourage them to ask their employer to look into business loans. We explain that the government simply wants to use payroll as a mechanism to get money to people. If they are not eligible for UC, they have very few, if any, short term options.

- People who started a new job but too late to qualify for the scheme. The government’s move to extend the scheme to those on PAYE on or before 19th March is positive and we have shared this news on our website.

- People with savings above £16,000. Some of these may qualify for New Style JSA or ESA, and we encourage them to apply, but these are typically paid at a much lower rate than UC as they are payments to the individual rather than the household. We have called for the government to increase the saving limit to £50,000 for twelve months.

- People with No Recourse to Public Funds can qualify for the furlough scheme or the Self Employed Income Scheme. However, for those that do not meet the criteria for these schemes there is no support of any sort. During the COVID-19 crisis they do not have the option to return to their home country, putting them at risk of destitution.

- Students whose parents do not meet their support obligations often support themselves through work. Some may be able to qualify for the furlough scheme or the Self Employed Income Scheme. For those who do not qualify for either scheme, there is no benefit support. The vast majority of students cannot claim Universal Credit or means-tested benefits. They too are at risk of destitution.

Currently, there is only discretionary support from the third sector for those without recourse to any support. This is often hard to find and provision is geographically patchy.

- Many appear to come to Policy in Practice without checking the government’s own information and advice pages, indicating the government communications could be clearer. We think councils, utility companies, banks and other institutions should be encouraged to point people to calculators like ours. As well as giving much needed advice to people early this approach helps frontline organisations to triage their support efforts where they are most required.

The survey responses were divided into nine key themes, one of which was the need to understand the complexity of the benefits system. Policy in Practice’s free Benefits Calculator helps people understand eligibility before making a claim http://www.betteroffcalculator.co.uk/free

Other Policy in Practice evidence submitted

- Universal Credit has shown flexibility and resilience in a way that the legacy system could not have matched. The committee should look to improve Universal Credit but move away from calls to scrap it or return to the legacy system.

- A number of council teams have reported difficulties in being able to access their benefit systems remotely while working from home. Councils may need funding to provide the necessary IT infrastructure.

- The furlough and self-employed schemes operate effectively as a temporary parallel benefit scheme run by HMRC. The increased generosity of these schemes relative to Universal Credit will need to be addressed if the measures are extended into June.

- Claimants missing out on furlough payments because their employer won’t operate it feel left out. The power lies with the employer in this scheme.

- The benefit cap limits of £1,667 outside of London and £1,916 in London per household compare poorly to the Treasury limit of £2,500 per month per person. The furlough scheme and SEISS have been put in place because people are unable to work through no fault of their own. We would argue that this is also true of means-tested benefit recipients subject to the benefit cap.

- The benefit cap only actually applies to those with children or privately renting. As support for renters is already capped through the LHA, the benefit cap primarily affects the level of support for children. In 2018 analysis by Policy in Practice found that 70% of the 2 million low-income families at risk of the 2-child limit if they have another child were in work. These are the families now reliant on means-tested benefits and so subject to the two-child limit for support. We argue that The two-child benefit limit and the benefit cap should be suspended (or at least increased to £2,500 per month) for the duration of the pandemic.

Policy in Practice’s recommendations to the Work and Pensions Committee

Policy in Practice makes three main recommendations to make the benefit system more supportive to claimants, and better able to support the country through this pandemic. We call for:

- The savings limit in Universal Credit to be suspended for the next twelve months, so people renting and/or with children that have saved over £16,000 are eligible for the same support as those without savings, and those on tax credits with no current income can be moved onto Universal Credit.

- The two-child benefit limit and the benefit cap to be suspended (or at least increased to £2,500 per month) for the duration of the pandemic, so people unable to work can access the similar levels of support to those on the furlough scheme.

- The increased generosity of the welfare system to be maintained after April 2021 to ensure we have a welfare safety net suitable for all.

The Coronavirus pandemic throws new light on the social security system

We recommended that the committee seek the government’s views on what this crisis means for the structure and purpose of the social security system overall.

We have huge sympathy for people who are coming into contact with the benefit system for the first time. The system is less generous than people have been generally led to believe, and though the simplification of six benefits into one is welcome, people are often still unsure of the rules and where to claim. This pandemic has highlighted the need for simple claim procedures and the provision of support for those that require it.

The current collective crisis that is driving people to rely upon the means-tested benefit system now is, in our view, no different to the personal crisis faced by people who were reliant upon the system before. Many of the holes in the provision and paucity of support have been addressed in response to the current crisis – emergency increases in UC basic allowances and in housing support for example. We need to ensure a reasonable safety net in the future for the many who will be dependent upon benefits once this crisis is over.

Join our next webinars

- Wednesday 6 May: Recap of the major benefits changes and Coronavirus (COVID-19)

- Wednesday 20 May: Coronavirus – stories from the frontline