What the changes to advance payments mean for low-income households

Janet Harkin Published on 01st October 2019

This month the Department for Work and Pensions (DWP) will reduce the maximum rate at which a payment advance is repaid in order to help ease the financial hardship experienced by some Universal Credit recipients. Repayment of the advance had previously been capped at 40% of the monthly Universal Credit standard allowance, and from October 2019 this will be reduced to 30%.

In this blog post we look at the numbers behind advance payments and ask whether the new measure, though welcome, goes far enough to secure the financial resilience of low-income households.

Lowering the cap for paying back advance payments is good news

Debt is already a rising concern. New Research by Policy in Practice shows that 14% of people yet to move to Universal Credit have insufficient savings to cover the five week wait and are already in debt or struggling to pay their bills before they move to Universal Credit. In the first 6 months of 2019, debt charity Step Change was contacted by a new client every 48 seconds as over 330,000 people turned to them for help with their debts.

The built in delay for the first payment of Universal Credit, known as the 5 week wait, can compound these debt issues as household’s day-to-day living costs still need to be met throughout the 5 week wait, even if no money is coming in. The advance payment was introduced to help families to manage the costs of transitioning to Universal Credit. It has been taken out by 850,000 households.

The proposed changes to repayment levels for the advance will ease the pressure from ongoing repayments which at the moment can last up to twelve months. However, by reducing the repayment rate from 40% to 30% without immediately extending the repayment period will reduce the advance available to families. This could put some household finances under greater pressure.

How the changes to advance payments affect people

At the moment 14% of people claiming Universal Credit are repaying more than 30% of their standard allowance. This new measure will be welcomed because it will help these households. A single person will gain by £32 a month and a couple over 25 will be £50 a month better off, as shown in the table below. In addition, from October 2021, the repayment period for these deductions will be extended from 12 to 16 months, giving hard-pressed families longer to pay.

| Single person | Couple |

|---|---|

| 40% of £317 = £126.80 | 40% of £498.89 = £199.56 |

| 30% of £317 = £95.10 | 30% of £498.89 = £149.67 |

| £126.80 - £95.10 = £31.70 | £199.56 - £149.67 = £49.89 |

Case study: Sarah

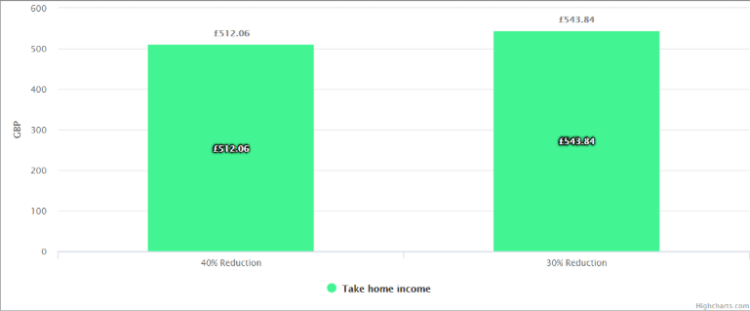

Using Policy in Practice’s Better Off Calculator it is possible to model how the change in the reduction rate from 40% to 30% affects an individual household. In this example, Sarah, a 30 year old single mother, is eligible for the maximum standard allowance of £317.82. Figure 1 shows Sarah’s take home income, after household costs have been included, at both the 40% and 30% reduction rates. The shift from 40% to 30% will give her an additional £31.78 take home income a month, boosting her financial resilience.

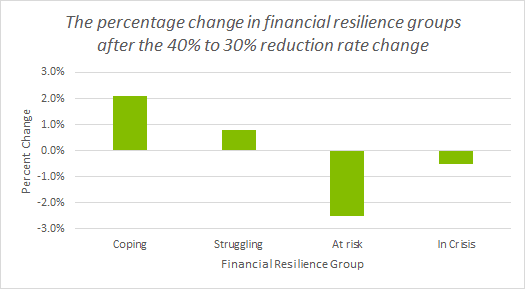

Using data from the Family Resources Survey we also analysed the impact of the reduced deduction rate at a national level. Using our financial resilience index that looks at the household’s income against housing and other essential costs we can see the impact that the change to the 30% reduction rate has, nationwide. Figure 2 illustrates that, with the change applied, the number of households with a shortfall decreases by 2.5% and 0.5% respectively. Overall, this appears to be a promising step towards tackling household debt in the UK.

Increasing the recovery period from 12 to 16 months also needs to happen now

Despite this relatively positive picture, there is room for improvement.

Reducing repayment levels without increasing the recovery period now ultimately means that some households will receive a lower advance payment. This is because advance payments are capped at the minimum level of the anticipated Universal Credit award, or the maximum repayment level multiplied by the maximum number of months for recovery, whichever is lowest.

At the moment, recovery of an advance payment occurs over a 12 month period. This is not due to be extended until October 2021. As a result, the maximum advance amount will fall from 40% of the standard allowance multiplied by 12 months, to 30% of the standard allowance multiplied by 12 months, reducing the maximum advance amount available to some households. The case study on Tom, below, illustrates this.

Case study: Tom

Tom’s full Universal Credit award is £1,600 a month, of which £317 is his standard allowance. He requests an advance payment. He receives his maximum repayment amount of £1,522, which is 40% of his advance payment amount spread over twelve months, as it is lower than his Universal Credit award. However, from October 2019, Tom’s maximum repayment amount will be reduced to 30% of his standard allowance. This means that the maximum advance Tom can receive will be reduced by £381 to £1,141.

In the worst case scenario faced my many, Tom’s advance will be reduced from £1,522 to £1,141 and he may need to take out further loans to make up the difference whilst waiting for his first Universal Credit payment. These further loans will need to be recouped in the months following the transition to Universal Credit, alongside his advance repayments, thereby cancelling out any extra income. Tom’s total debt repayments may therefore see little change, or even increase. Unlike the advance repayments to DWP, these additional third-party repayments are likely to carry higher interest so Tom ends up experiencing greater ongoing financial pressure with 30% advance deductions over 12 months than he would have with 40% deductions over 12 months.

| September 2019 | October 2019 | October 2021 |

|---|---|---|

| 40% of £317 = £127 | 30% of £317 = £95 | 30% of £317 = £95 |

| £127 multiplied by 12 months recovery period = £1,522 | £95 multiplied by 12 months recovery period = £1,141 | £95 multiplied by 16 months recovery period = £1,521 |

Policy in Practice finds that more than 9% of households yet to move onto Universal Credit will see an average reduction to their maximum advanced payment of £215. However, if the DWP introduced the planned extension of the repayment period from 12 months to 16 months now, and not in 2021, the lower deduction rates would be far more effective at boosting the financial resilience of low income families.

Changes to advance payments are welcome but they’re not the final fix

Debt is a serious and growing issue for low-income households and the move to reduce the repayment rate is a welcome step in the right direction. But the DWP should consider the implications for those households that will receive a lower advance as a result and bring forward the start date for the extension of the repayment period. We also believe that payment advances are not the cure for poverty during the wait for benefit support. The use of Advance Payments is ultimately creating additional debt for already struggling households.

Policy in Practice recently published research, commissioned by the Joseph Rowntree Foundation, analysing the resilience of households and the transition to Universal Credit. The report identified seven factors that drive financial resilience and gave four recommendations:

- A targeted grant in place of the Universal Credit advance payment for those households clearly struggling because of the transition to Universal Credit

- A two-week run-on of Child Tax Credit, paid through the Universal Credit system, to help families with children

- Fortnightly payments of Universal Credit, starting with an initial payment at two weeks based on the estimated monthly award amount

- Greater flexibility in processes such as the recovery of overpayments and advances, claim verification and backdating, as called for by claimants, to help people to manage the transition to Universal Credit

The government has indicated that austerity is ending and the appointment of Therese Coffey, the new Minister for Work and Pensions, is a valuable opportunity to introduce changes that will help struggling low-income families now.