Universal Credit and income volatility: how councils can help

Mary-Alice Doyle Published on 20th July 2023

Universal Credit can make household income volatile. Policy in Practice is analysing data to see how this affects households’ financial lives and find ways to help families better manage this volatility. Our goal is to give councils the tools to help families to stabilise their finances.

In this blog we look at why families on benefits experience income volatility. We also introduce our new research project that aims to understand more about income volatility and the practical steps that can be taken at a local level to reduce these pressures on household finances.

Households on low incomes can experience income volatility, working or not

Having volatile earnings makes it difficult to budget which means that families are at higher risk of falling into problem debt and financial crisis.

We often hear about the issues of volatile, unpredictable income in the context of the labour market when the ‘gig economy’ and zero hour contracts are discussed. Households receiving benefits experience substantial income volatility too. This is even more the case in recent years as, over time, the benefits system has become less able to counteract swings in employment income.

With the value of benefits so low, nine out of ten Universal Credit recipients are going without essentials, leaving households with very little scope to cushion fluctuations in their income with savings.

Three reasons why households on benefits experience income volatility

There are three main reasons why income fluctuations for households on Universal Credit are likely to be greater and more unpredictable than for other households:

- The interactions of Universal Credit (UC) with employment income

- The interactions of UC with other income sources

- Deductions from Universal Credit or sanctions

Reason 1: The interactions of Universal Credit (UC) with employment income

Around two out of five UC recipients are working. They are often employed in low-wage jobs, paid on a weekly rather than monthly basis, or are self employed, with variability in their earned income.

The way benefits are administered can add an extra element of variability. This happens because UC is paid monthly in arrears. This diagram illustrates how that can happen:

For example, say I am employed on a casual basis at minimum wage and I receive UC. Usually:

- I work 20 hours a week

- I earn £832 per month from my job

- I get £882 from UC

My total income is £1,714 per month.

However, at the end of December and in early January, I took two weeks off and earned only £411 in that pay period.

Because there is a whole month between my reduced pay in January and UC adjusting upwards in response, I have to wait until the end of February for my UC payment to increase in response.

This means I have a 25% drop in my income month-to-month in January, then a 50% increase in February.

This simple example shows how a recipient who usually gets paid the same amount can experience occasional fluctuations.

People with more frequent volatility in their earnings and variable pay periods can experience even more fluctuations.

Reason 2: The interactions of UC with other income sources

Income from other sources may interact with UC in a similar way to the above example with earnings.

Some common income types are often paid at differing frequencies, for example:

- Carers Allowance is usually paid weekly

- New Style ESA and JSA are paid fortnightly

- Pensions may be paid at differing frequencies such as weekly, four weekly, monthly, quarterly or annually. According to the latest FRS data 11% of private pensions are paid quarterly or less frequently meaning many households may be in this situation

Reason 3: Deductions

Many households receiving benefits have deductions such as sanctions or repayments of advances that reduce their take home pay significantly.

Sanctions in particular affect a rising number of UC recipients, some 114,000 claimants according to the latest figures. In addition, a large share of recipients have other deductions taken from their UC payment to repay loans, overpayments or pay down debts.

The UC data that we work with suggests that around half of UC claimants have some type of deduction from their monthly award, though this may vary across localities. Such deductions can accentuate income volatility which is why we plan to do more analysis to understand how deductions vary from month to month within a household.

Income volatility makes it harder for households on the lowest incomes to budget month to month

The benefits system is supposed to provide payments that vary depending on a household’s circumstances. We expect the award to decrease when other income increases and it would be surprising if it didn’t given that the point of a benefits system is to provide a safety net.

The issue here is the timing.

Because of the way UC is administered it can exacerbate short term income volatility. Crucially, it means that a lump sum payment or a short term change in employment income can reverberate into the following months which makes it harder for families to budget month to month.

This is a real issue because households in this situation risk going without essentials, or falling into problem debt.

We already see household borrowing such as credit cards and payday loans increasing over the past year, alongside an increase in the number of people seeking debt advice.

To date little analysis on these income fluctuations has been done, because until now it wasn’t possible. Most data sources available to researchers cannot tell us anything about within-year income volatility.

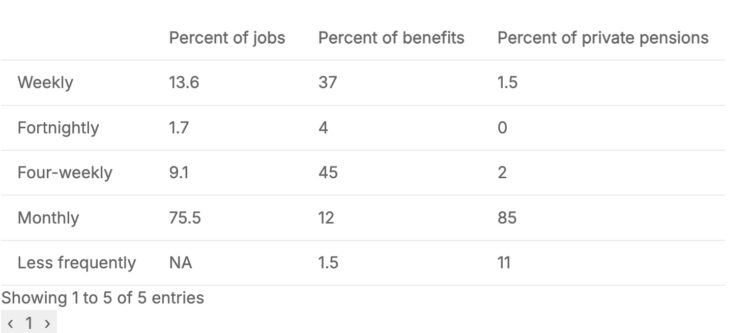

Survey data can tell us how frequently people receive different types of income. This is a first step to understanding the issue because it makes clear that, while the majority of people are paid monthly, there are still millions of households with more or less regular payments, as shown in the table below.

However, survey data cannot tell us how payment frequency interacts with UC, and the impact on households’ financial security.

A better understanding of these issues is key to developing policy that works for people, where all parts of government work together to help alleviate cost of living pressures.

Table: Payment frequency, by source of income

| Percent of jobs | Percent of benefits | Percent of private pensions | |

|---|---|---|---|

| Weekly | 13.6 | 37 | 1.5 |

| Fortnightly | 1.7 | 4 | 0 |

| Four-weekly | 9.1 | 45 | 2 |

| Monthly | 75.5 | 12 | 85 |

| Less frequently | NA | 1.5 | 11 |

Sources: Jobs data from ONS ASHE 2017; Benefits and pension data from FRS 2020/21. Benefits include Universal Credit, ESA, JSA, IS, Housing Benefit, State Pension, Pension Credit, DLA, PIP, Carer’s Allowance, Attendance Allowance, Child Tax Credit, Working Tax Credit and others.

The current system may be fine for most households, most of the time. But when we are living through a cost of living crisis with more households living from payday-to-payday we need to know how the benefits system may be contributing to this, and how local and national policymakers could address this.

Call for research participants: How can local authorities and advisors help tackle income volatility

Local authorities have a rich source of administrative data that can be analysed to understand income volatility on low income households. The Low Income Family Tracker (LIFT) platform that Policy in Practice has built can help councils do this at a local level.

Councils can use LIFT to track household income and expenditure and target much needed support.

The ‘Next Month’s UC’ feature in the Better Off Calculator allows households and their advisors to predict how changes in earnings affect their UC award.

But we can do more.

This month we are launching a new project to scope out what administrative data can tell us about income volatility and practical work can be done at a local level to alleviate these pressures on household finances.

We are seeking leading local authorities to participate in this scoping project.

Please contact research@policyinpractice.co.uk to join our research project or call 0330 088 9242 to find out more.