Mind the benefit cap: why families are still falling through our welfare system

Zach Mills Published on 23rd June 2022

The government’s latest benefit cap statistics, released by DWP this week, reveal that around 120,000 families had their benefits capped in February 2022. New analysis from Policy in Practice shows that larger families cannot afford to rent anywhere in Britain without sacrificing money meant for food and daily living if they are affected by the benefit cap. This blog explores the benefit cap’s effect on families as living costs rise, and gives one potential solution that could ease the financial pressure being faced.

Lone parents are hardest hit by the benefit cap

From the latest official DWP statistics approximately 120,000 households are affected by the benefit cap. From these households:

- Nine out of ten benefit capped families had children

- Five out of ten benefit capped families had a child under five

- Two out of three benefit capped families were single parents

- One out of three benefit capped families were single parents with a child under five

The new statistics show that lone parents with three or more children make up nearly half of the capped caseload (42%). Intuitively, this makes sense as lone parents looking after children face higher barriers to work making it more difficult to become exempt from the benefit cap.

Households with multiple children are also likely to be receiving more benefit support and therefore be closer to the cap limit.

Recap: brief history of the benefit cap

In 2013, the benefit cap was introduced with three explicit aims. The first was to encourage more people into work. Secondly, the benefit cap aimed to restore “fairness” to the benefit system, and thirdly, it was intended to make financial savings.

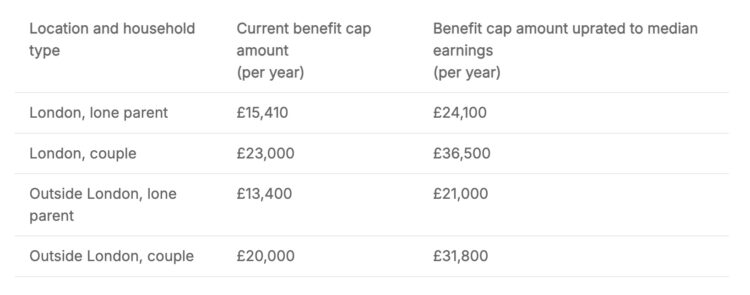

The benefit cap meant that households could not receive more than £26,000 a year in state benefits. This changed to £18,200 for single people with no children.

In 2016, as part of the government’s ongoing austerity measures, the benefit cap was lowered to £20,000 for households outside of London and £23,000 per year for households living in London. This changed to £13,400 for single people with no children outside the capital and £15,410 for single people with no children inside.

In 2022 the benefit cap remains at this level and has never been increased in line with inflation. The original baseline for the cap, median earnings, has risen by 18% during this time and now stands at £31,800 per year (£611 per week) for full time employees.

In 2019 the Work and Pensions Select Committee concluded that the policy had performed poorly against all three of its stated aims. Only 5% of recipients had been judged to move into work because of the cap.

More recently, the government has come under criticism for increasing benefit rates by just 3.1% in April 2022 rather than the 8% needed to keep up with rising costs. However, households affected by the benefit cap will not even receive the 3.1% increase to their benefit award.

Instead, these households are tasked with living on less than is needed to pay for rent, utility bills, food and other living costs, by the government’s own definitions. Higher prices of all of these things will be significantly harder to meet for those families already living on an inadequate income.

The recent one-off £650 Cost of Living Payment for people on means tested benefits does not count towards the benefit cap and is a welcome boost to these households’ income. However, this is a short term solution and does little to help these families become self-sufficient in the long term.

Additionally, without reform, benefit capped households will still not receive any extra income when benefits rates are uprated in April 2023 in line with the Consumer Price Index (CPI) in September.

Benefit capped families struggle to afford private rents

In the midst of rising rents and living costs, finding accommodation within the Local Housing Allowance (LHA) is a significant challenge for households relying on housing support. The LHA rate is used to calculate how much housing support a household renting privately may be eligible for.

The LHA rates are based on private market rents paid by tenants in the broad rental market area (BRMA) and the household composition. In March 2020, LHA rates were re-aligned with the 30th percentile of market rents, having previously been frozen since 2016. LHA rates have once again been frozen at their current rate, meaning they will again quickly fall below the 30th percentile.

In previous years, people on lower incomes could be protected from higher rental costs via the provision of social housing and benefits that covered most of their housing costs. Now that access to social housing is harder, many low income families are exposed to higher housing costs in the private rented sector.

For households affected by the benefit cap rent at the LHA may still be unaffordable. If a household’s benefit income exceeds the benefit cap their housing support will be reduced accordingly. These households either have to rely on discretionary support from their council in the form of Discretionary Housing Payments (DHPs) or choose between paying rent and having enough money for food and energy bills.

Policy in Practice carried out an analysis to assess the affordability of each BRMA across Britain, within the current benefit cap limits. Within this analysis, a BRMA was deemed affordable if:

- a household could afford to pay the rent at the LHA rate within their benefit cap limit and

- without having to use money from the personal allowance of any means-tested benefits or any other benefit income.

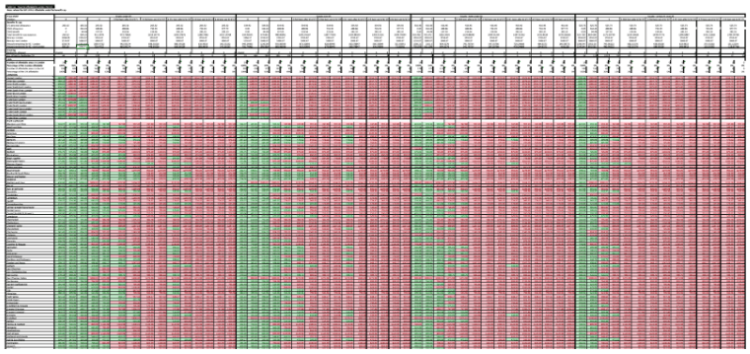

Analysis shows few places where benefit capped families can afford to privately rent

We modelled the affordability of housing for families affected by the benefit cap for all 191 broad rental market areas (BRMA) across Britain, for a wide range of household circumstances. This included families who were single, couples, under 25, over 25, no children and up to four children.

In the heat map below the columns represent the different family circumstances and the rows the 191 BRMAs. The green areas denote affordable places and the red unaffordable. We can see the majority of BRMAs are unaffordable.

If you work in a local authority housing or homelessness team and would like access to the spreadsheet email hello@policyinpractice.co.uk

Benefit capped families with more than two children can’t afford to privately rent anywhere in Britain

Our analysis shows that families, either lone parents or couples, who receive benefit support for more than two children cannot afford to rent anywhere in Britain if they are affected by the benefit cap. Due to the 2-child limit a household would not receive benefit support for any third or subsequent child born after April 2017.

Given the current demographic make-up of the benefit capped caseload, half of the households affected by the benefit cap cannot afford to rent anywhere in Britain without using money from their personal allowance to pay rent.

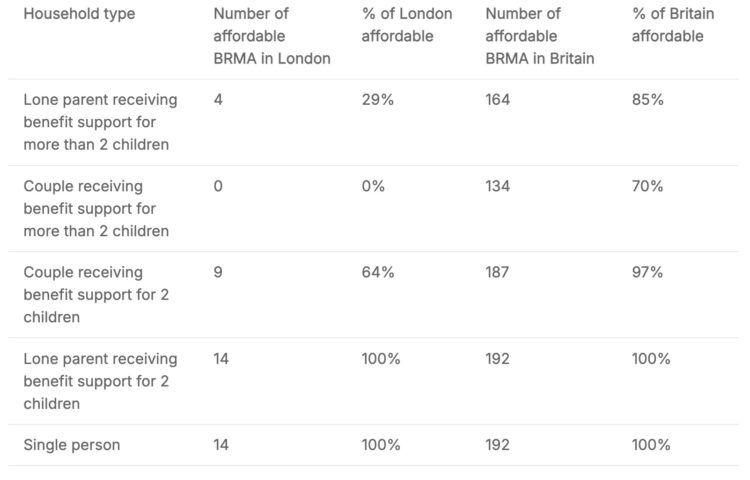

The number of Broad Rental Market Areas (BRMA) that are affordable for each type of benefit capped household

In London, we can see that a family with any number of children affected by the benefit cap cannot afford to rent privately without using money from their personal allowance to pay rent.

Elsewhere, lone parents with two children can only afford to rent in half of the areas in Britain and couples with two children can only afford to rent in 10% of Britain.

Prior to the current cost of living pressure, the Supreme Court ruled that no household should be expected to use money from the personal allowance of any means-tested benefits to cover a gap between rent and housing support (Samuels v Birmingham City Council, 2019). In the current context, the personal allowance of means-tested benefits is barely sufficient to cover food and energy bills, let alone contribute towards covering rental costs.

Solution: Uprate the benefit cap in-line with median earnings

A possible solution to ease the affordability of privately rented accommodation would be to uprate the benefit cap limits in line with the current median earnings. The latest ONS figures show that median earnings in the UK are now £31,800 per year for full time employees. Policy in Practice has explored what the benefit cap rates might look like if the national benefit cap amount was realigned to median earnings.

Comparison of benefit cap rates if the benefit cap amount was realigned to current median earnings

Increasing the benefit cap to match current median earnings improves the picture for households living under the cap, as shown in the table below.

The number of Broad Rental Market Areas (BRMA) that are affordable for each type of benefit capped household if the benefit cap was uprated in line with median earnings

London is still mainly unaffordable for larger families. However, families with more than two children could now afford to rent in over 70% to 85% of Britain compared to nowhere within the current benefit cap.

Ease the financial pressures faced by benefit capped families

Although not a perfect solution, increasing the benefit cap in line with median earnings allows the policy to still work towards its aims of encouraging work, creating fairness and reducing welfare spending (compared to no cap at all).

It would also mean fewer households would need to use their personal allowance of means tested benefits to cover the gap between rent and housing support.

Crucially, it will give families that are unable to become exempt from the benefit cap a realistic chance of being able to afford private rented accommodation in Britain and have the money to provide for their children.