Future proofing Council Tax Support for LGR and the 2027 policy reset

Deven Ghelani Published on 04th March 2026

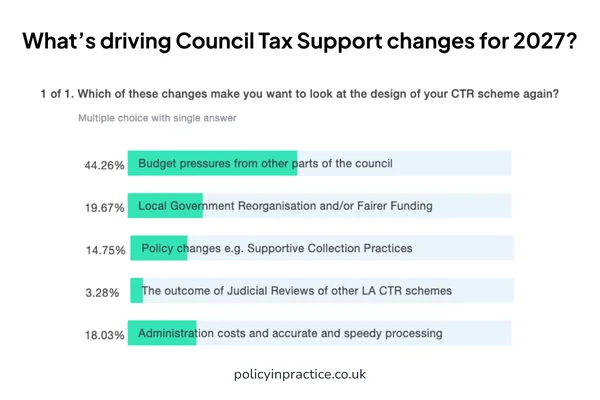

At our recent webinar on Council Tax Support scheme modelling we asked attendees what’s driving scheme changes in their local authorities.

It was clear from the poll results that budget pressures from other parts of the council are the main driver prompting scheme review, but financial constraint is not acting alone.

Attendees also highlighted:

- Local Government Reorganisation and/or Fairer Funding

- Administration costs and the need for accurate, timely processing

- Policy change, including the Child Poverty Strategy and supportive collection practices

- The outcome of recent judicial reviews of other local authority CTR schemes

These drivers for scheme changes reflect a wider shift in the context for Council Tax Support in 2027. Scheme design is being influenced by policy reforms, operational pressures and greater scrutiny, alongside affordability.

Lyndsay Sayer, South Norfolk and Broadland Councils, joined Rory Ewan and Deven Ghelani, Policy in Practice, to explore how these factors are influencing both the design of support schemes and how they are being administered day to day. Listen back to the webinar and view the slides here.

Record arrears and a changing environment for Council Tax support

Council Tax arrears in England have reached a record £6 billion, up from £3.5 billion a year before the pandemic.

Local authorities see this reality reflected in rising demand for hardship support, stretched collection teams, increased pressure on local welfare assistance, and difficult conversations with residents who simply cannot pay.

For over a decade, councils have adjusted their local Council Tax Reduction (CTR) schemes by tightening maximum awards, introducing income bands, introducing caps to the council band of properties and non-dependant deductions. These changes were often driven by necessity: funding reductions, welfare reform, political priorities and the ongoing pressure to balance budgets.

But the changes needed for CTR schemes for 2027 go beyond incremental adjustment.

Budget pressures remain significant; 44% of attendees at our recent webinar cited them as the primary reason to revisit their Council Tax support scheme. Yet financial constraint is now only one part of a much wider structural shift.

Local Government Reorganisation (LGR) will require newly formed authorities to operate a single, unified CTR scheme from day one. The removal of the two-child limit, changes under the Universal Credit Act 2025, the end of managed migration, and the forthcoming statutory guidance linked to the Child Poverty Strategy all significantly alter the landscape in which CTR schemes operate.

At the same time, recent judicial reviews have heightened the risk of legal challenge where schemes treat certain income types differently or apply reductions without clear justification.

As Rory Ewan, Senior Policy and Data Analyst at Policy in Practice, put it during the webinar:

“In 2026, going into 2027, there’s really a changing landscape of how local authorities should be designing their CTR schemes. There’s not just the budgetary pressures anymore – there’s policy changes, judicial reviews to take into account and there’s lots more guidance to consider when you’re designing your scheme.”

CTR can no longer be treated as a standalone benefits policy. It sits at the heart of financial sustainability, inequality reduction, child poverty strategy, collection performance and corporate governance.

For councils preparing for LGR, reviewing Council Tax support schemes will be unavoidable. For those outside reorganisation, welfare reform and rising demand still point in the same direction.

The issue is not simply whether to revisit CTR in 2027, but how to design a scheme that remains fair, lawful and sustainable over the years that follow.

What policy changes coming in 2027 mean for Council Tax Reduction design now

Several developments coming into effect over the next two years will directly affect how Council Tax Reduction schemes operate.

Changes to Universal Credit, including the removal of the two-child limit and reforms under the Universal Credit Act 2025, will alter income patterns within CTR caseloads. For authorities operating income banded schemes, this interaction matters. Where band thresholds are closely aligned to Universal Credit elements, households may move between bands as UC rules change, sometimes resulting in reduced awards despite no change in underlying circumstances.

The completion of managed migration will mean Universal Credit becomes the primary gateway benefit for almost all working age residents. As UC caseloads increase, so too will Universal Credit Data Share (UCDS) notifications. For many councils, this already represents a significant administrative demand.

Recent judicial reviews have also clarified expectations around consultation, proportionality and the treatment of income within Council Tax Reduction schemes. Decisions relating to double counting and transitional protection underline the need for scheme design to be robust and defensible.

Alongside this, the Child Poverty Strategy places greater emphasis on supportive collection practices and the consideration of socioeconomic disadvantage. Council Tax Reduction is explicitly recognised as part of a wider approach to reducing inequality.

Taken together, these changes reshape the context in which Council Tax Reduction schemes are designed and administered.

Bringing Council Tax Reduction schemes together under LGR

Local Government Reorganisation adds another layer to the 2027 policy context. New councils will need an operational CTR scheme on day one, which will have an impact on the winners and losers for residents and local authorities.

Where existing district schemes differ, for example in maximum awards, income bands, earnings disregards or non-dependant deductions, harmonisation is more than a technical exercise. It requires decisions about distributional impact, and political priority across a larger and more diverse population.

As Lindsay Sayer, Partnership and Innovation Senior Manager, South Norfolk and Broadland District Councils, discussed during the webinar, the differences between schemes are often subtle yet significant. One authority may operate restricted bands while another does not. One may treat child maintenance differently. Earnings disregards and non-dependant deductions may vary. Individually, these differences reflect local choice. Combined under LGR, they create complexity that must be resolved.

The challenge is therefore less about creating a single scheme, and more about deciding how that scheme should balance fairness, cost and administrative practicality across the new geography.

Demographics will vary. Caseload profiles will vary. Financial exposure will vary. A feature that is broadly neutral in one area may have a more pronounced effect in another. Without modelling, these impacts can be difficult to anticipate.

As Lindsay reflected during the session, bringing schemes closer together means balancing affordability, fairness and administrative simplicity, and you can only have two of the three.

“You can’t focus just on budget,” Lyndsay noted. “You can’t ignore what members want to protect, and you can’t design something the team simply can’t administer.”

In this context, LGR becomes more than a structural milestone. It is an opportunity to step back and examine how Council Tax Reduction operates in practice and whether legacy design choices remain aligned with future objectives.

Two councils, one team: practical lessons in aligning Council Tax Reduction schemes

The experience of South Norfolk and Broadland District Councils provides a practical example of how Council Tax Reduction schemes can be brought closer together.

The two councils operate with a shared officer team but remain sovereign authorities, each with its own Members and Council Tax Reduction scheme. The work to align their schemes was not linked to Local Government Reorganisation. Instead, it arose from the practical challenge of operating two different Council Tax Reduction schemes within a single shared team.

Although the schemes appeared similar at a high level, there were important differences. One included restricted bands while the other did not. Child maintenance was treated differently. Maximum awards varied. Earnings disregards and non-dependent deductions were not aligned. These variations meant the team effectively had to administer two distinct policies for what they described as “one set of customers.”

To address this, the councils worked with Policy in Practice to model potential CTR scheme changes. Using detailed household level data, they were able to assess:

- The financial impact of alignment for each council

- The social impact of changes on different resident groups

- Whether proposed changes would adversely impact particular cohorts

- The overall cost implications of scheme adjustments

This modelling supported discussions with Members by providing clear evidence of the distributional and financial effects of potential changes.

In 2024, the councils again used modelling when seeking to increase their maximum award from 84% to 87%. Members wanted to increase support in response to cost of living pressures, but there was no additional budget available. By adjusting non-dependant deductions and earnings disregards, the councils were able to increase the maximum award while maintaining overall budget neutrality.

As Lindsay reflected during the webinar:

“Having that evidence base is always just completely invaluable going through any governance process and persuading people who may be a little bit more dubious about what you’re trying to do.”

The approach taken by South Norfolk and Broadland Councils demonstrates how evidence-led modelling can support scheme alignment and redesign where multiple policies need to be brought together.

Managing Universal Credit data: turning UCDS pressure into operational resilience

Much of the discussion around Council Tax Reduction focuses on scheme design. During the webinar, however, the conversation also turned to administration and the growing impact of Universal Credit Data Share (UCDS) notifications.

At South Norfolk and Broadland, the CTR scheme was written so that Universal Credit data could be treated as a new claim. If a UCDS record indicated that a resident was entitled, the council could make an award without requiring a separate application.

As Lindsay explained, this approach was intended to simplify the process for residents:

“If we get a UC record in that says they’re entitled, we can just pay them.”

However, the volume of data share records has increased significantly over time.

Each notification still requires review to determine whether an award needs to be created or amended. Even where a resident is not ultimately entitled, the record must be assessed.

As Lindsay described:

“We have to look at all the records that come in to see if the customer needs to have their award changed or if it needs to have a new award… and it’s absolutely killing us.”

This reflects a wider operational challenge. As Universal Credit has become the main working age benefit, CTR administration is increasingly driven by automated data flows. Where systems cannot process those notifications end to end, manual review absorbs officer time.

In response, South Norfolk and Broadland have been working with Policy in Practice to explore whether council tax liability data and UCDS information can be combined to identify which records genuinely require action, allowing teams to focus on higher priority cases.

Using data to increase CTR take up and reduce avoidable arrears

In response to the growing administrative burden of UCDS notifications, South Norfolk and Broadland began exploring whether data could be used more effectively to filter cases before they reached officer review.

As Deven Ghelani explained during the webinar, Policy in Practice’s LIFT platform can now incorporate council tax liability data alongside Universal Credit Data Share information. This makes it possible to assess likely eligibility for Council Tax Reduction before manual processing begins.

The objective of the project was to identify which cases required valuable officer attention, to enable, not replace, officer decision making.

The intention was twofold:

- Reduce administrative pressure by removing unnecessary manual checks

- Improve take up of Council Tax Reduction by identifying households that are entitled but not yet receiving support

In early analysis:

- 99% of UCDS cases were successfully linked to council tax liability data

- In over 90% of cases, the assessment correctly identified whether a household was eligible for CTR

The work has enabled officers to focus on the cases most likely to result in an award, while filtering out notifications where no action was required.

As Deven noted during the session:

“If you can get someone onto CTR you’re improving their wellbeing, streamlining the process for yourself, saving resource, but saving at the back end as well because there’ll be less to collect, lower collection costs and you’re helping people build their financial resilience.”

This shifts the framing of CTR from a reactive discount to a preventative intervention. By identifying eligibility earlier, councils can reduce avoidable arrears, limit the need for hardship funds, and strengthen collection performance.

Independent modelling for informed CTR scheme design

For councils affected by Local Government Reorganisation, review of Council Tax Reduction schemes is unavoidable. A single scheme will need to be agreed and operational from vesting day.

For others, the trigger for CTR scheme redesign may be policy change, administrative pressure or judicial scrutiny. In all cases, scheme design is increasingly exposed, financially, legally and operationally.

Where schemes are being aligned, detailed modelling provides clarity on distributional impact before decisions are taken. Where administrative pressure is growing, better use of data can reduce unnecessary workload and improve take up.

In both cases, robust analysis and clear evidence underpin effective governance.

Policy in Practice has spent over a decade modelling Council Tax Reduction schemes across England, supporting councils through localisation, welfare reform and now LGR. The work highlighted in this session, combining household level modelling with operational data analysis, reflects a continued focus on evidence led design.

As 2027 approaches, councils reviewing their schemes will need confidence that decisions are fair, lawful and financially sustainable, backed by independent, clear and defensible analysis. Policy in Practice is happy to help.

Next steps

- Listen back to the full webinar: Council Tax Reduction: Practical approaches to policy reform and supporting the most vulnerable

- Download our report: Rising arrears, shrinking support: Five years of CTR trends: A path to better Council Tax Support schemes

- Read our case study: How Waltham Forest delivered £2.3m savings through Council Tax Reduction Scheme modelling