Autumn Statement 2023: Uprating benefits – the long view

Jack Rowlands Published on 27th November 2023

In the second of our Autumn Statement 2023 blogs we explore the announcement to uprate working age benefits using the September CPI figure of 6.7% while maintaining the triple lock on the state pension to increase it by 8.5%. Both increases are due to come into effect from April 2024.

Our analysis shows that benefits are failing to keep up with inflation and means tested benefits are worth 8.8% less now than in 2012.

The welcome Autumn statement’s announcement on uprating benefits is the largest single increase to working age benefit rates since 2010.

Increased benefit payments are likely to be welcomed by families struggling with the cost of living crisis, and the increased rate of 6.7% was higher than expected, suggesting the government has heard the welfare sector’s concerns.

As costs increase for us all, bringing benefit rates in line with cost increases each year would ensure low income households are better placed to keep up with increases in basic costs. However, benefits are not uprated in line with increased costs, leading to an ongoing shortfall in low income household finances.

The government’s estimates have found the combination of working age and pension age increases will impact 19.5 million households in Great Britain. However, despite the unexpectedly higher rates of increase, benefit payment rates continue to trail behind inflation.

Uprating benefits by 6.7% is not enough to keep pace with inflation

Uprating working age benefits by the September 2023 CPI rate of 6.7% is a positive move that helps households facing the cost of living crisis.

However, past benefit rate freezes mean that the value of benefits has fallen below the rate of inflation since 2013.

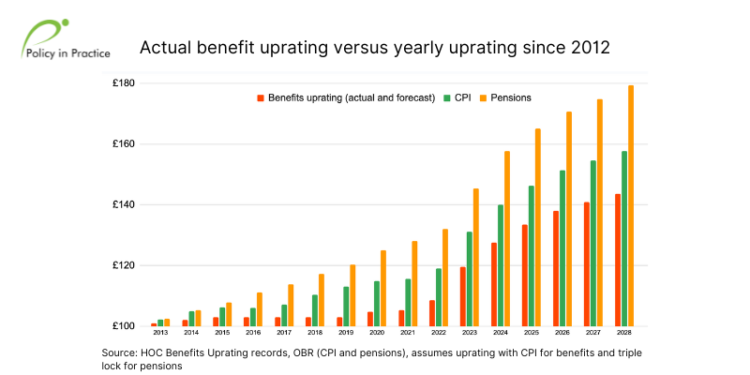

The chart below shows actual benefit uprating versus yearly uprating since 2012 and reveals that benefits continue to be outpaced by inflation over the last decade, even when factoring in next year’s uprating decision. Benefit rates are not currently linked to any figures that represent the actual cost of living for these households.

Inflation fell to a low of 4.6% in October 2023 from a high of 11.1% in October 2022, but the impact of previous benefit freezes with the yearly uprating has meant that the finances of low income households still fall below the price rises of the last few years.

Low income households are hit hardest by inflation because most of their spending is on essential items such as food, housing and utilities. Food inflation is still 10.1% this year, energy bills will rise by 5% in January and water bills are expected to increase by 40% from 2024.

People on state pensions keep the triple lock while lowest income pensioners miss out on billions in benefits

Maintaining the triple lock and uprating state retirement pensions by 8.5% helps pensioners with the cost of living crisis, particularly those who rely only on state support. Although pension age benefits have continued to rise at a level higher than working age benefits pensioner poverty is still an issue.

The take up of Pension Credit and Attendance Allowance remains low amongst low income pensioners and, despite awareness raising campaigns by the government and Policy in Practice’s own targeted campaigns with local authorities that have increased Pension Credit take up, more can be done to support older people living on a low income. Data led campaigns can help target the most vulnerable and out of contact with local support services.

Policy in Practice calculated that 850,000 households are missing out on Pension Credit worth £1.5 billion a year. This can be worth an average of £3,500 a year for one household alone through Pension Credit, and more for older people who are disabled or carers.

Next analysis of Autumn Statement 2023 and the National Living Wage: Who benefits most?

Our next Autumn Statement 2023 blog looks at the National Living Wage, examining the increase to £11.44 which means that low paid workers will see a welcome boost to their wages.

This is one of the largest increases in the National Living Wage since it was introduced in 1999, and another increase likely to be welcomed by in-work households claiming benefits.

Tomorrow’s blog looks at how increased incomes are treated when taper rates are applied, and how households on Universal Credit may not feel the benefit of the full increase.

Read more

- Autumn Statement 2023: A step forward after many steps back

- How London used data to make pensioners £8 million a year better off

Join our free webinars

- Reducing barriers to work with data led campaigns on Wednesday 29 November. Details and registration here

- Policy review of 2023 and what 2024 may hold on Wednesday 6 December. Details and registration here