Low income households will still be worse off in April 2023 despite extra support

Alex Clegg Published on 12th December 2022

Uprating benefits by inflation, increasing the National Living Wage and further cost of living payments still won’t be enough to stop thousands of low-income families from being worse off in April, as costs continue to outstrip income.

Our new analysis of over 114,000 low-income households across six local authorities shows that the average low-income household will be slightly worse off in April 2023 than they were in February and November this year, even after benefits are uprated by 10.1%, the National Living Wage is increased to £10.42 and the next round of cost of living payments are made.

The discontinuation of the £400 energy rebate and the ongoing freeze of the Local Housing Allowance, coupled with rising rents, council tax, energy bills and household costs are projected to outweigh the increase in income from these measures, leaving thousands of households unable to meet their costs.

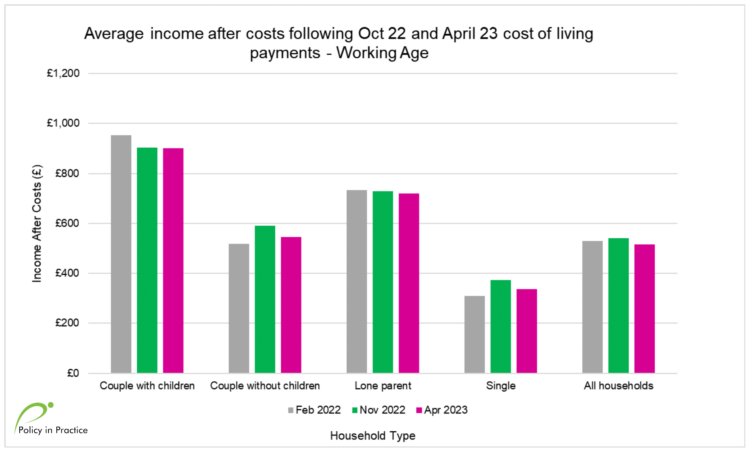

Low-income households will be slightly worse off in April 2023, despite benefit uprating

Policy in Practice conducted analysis on benefits administration data from six local authorities spread geographically around the UK, representing over 114,000 low-income households.

Household costs were estimated using the ONS Family Spending Workbook, with energy costs increased in line with the Energy Price Guarantee and other costs increased by projected CPI inflation figures for November 2022 and April 2023.

Council tax liabilities were increased by 5% and social rents increased by 7% to reflect the maximum they can go up by next year, whilst private rents were increased by 5.1% to reflect the latest OBR forecast.

We found that, on average, these low-income households will be slightly worse off in April 2023 than they were in both February and November, even after benefits are uprated by 10.1%, the National Living Wage is increased to £10.42, and the next round of cost of living payments are taken into account.

For our analysis the £900 and £650 payments to households on means-tested benefits were averaged over 12 months, to reflect the two six-monthly instalments of each payment. The £150 payment to households in receipt of a disability benefit and the £400 energy rebate to all households in winter 2022 were averaged over 6 months, to reflect a reasonable budgetary increase from these payments.

The average low-income working-age household was £12 per month better off in November than in February thanks to the first round of cost of living payments and the £400 energy rebate.

However the same household is set to be £13 per month worse off from April 2023 compared to February 2022 because:

- energy costs will rise by another 20%

- CPI inflation is projected to remain high at 8.9%

- Council tax liability is likely to increase by 5% and

- Rents are projected to go up by an average of 5.1%.

Worryingly, the analysis is likely to underestimate rising costs for low-income households because it does not account for regional differences in expected rent and council tax rises or the tendency for lower income households to spend a greater proportion of their budgets on categories such as food and fuel. These latter costs are rising in price faster than the overall CPI inflation rate.

Couples with children will be hit particularly hard as their real incomes are projected to fall by £53 per month from April. This is because the cost of living payments do not go as far for larger families. This highlights the challenge with providing flat-rate support regardless of household size.

For other household types disposable income is likely to remain similar between November 2022 and April 2023. This may be seen as a positive considering the context of the cost of living crisis. Benefits uprating, the Energy Price Guarantee and the one-off cost of living payments are doing their job of absorbing the majority of the cost increases caused by soaring inflation.

However, conversations surrounding benefits can often mask how much the value of benefits has fallen from acceptable standards of living.

Even before the current crisis, households on benefits have lost out to inflation for a decade. 10% of working age households in our dataset did not have enough income to meet their expected household costs in February 2022, and this is set to rise to 11% in April 2023. For single people, this figure is projected to be 14% in April 2023.

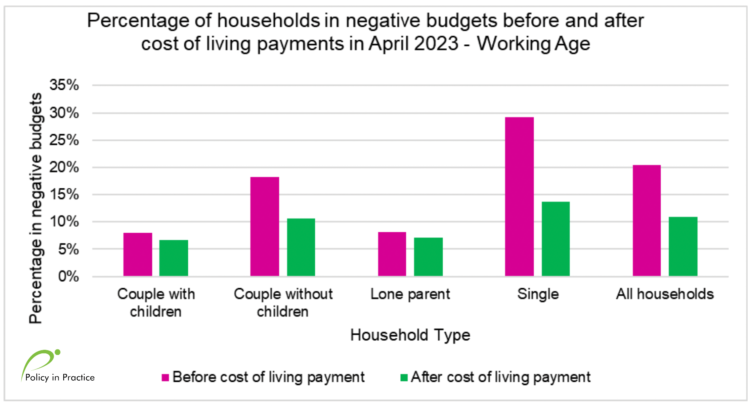

The cost of living payments are preventing thousands of families from being unable to meet their household costs

Despite the bleak outlook for April 2023 our analysis shows that the proportion of low income households that would be unable to meet their costs is almost halved from 20% to 11% because of the cost of living payments. This is particularly pronounced for single people, as the payments reduce the proportion in a negative budget from 29% to 14%.

The need for these payments to top up what people get from the mainstream benefit system highlights how inadequately benefit rates prevent people from falling into poverty, debt and homelessness.

Low-income families deserve certainty over their budgets, rather than having to hope the government continues to issue one-off payments to keep their heads above water. We argue that the cost of living payments should be replaced by a permanent increase to the level of benefits. This would also ensure that support was more proportional to household size and income.

The need for discretionary support to plug the gaps in the safety net is creating a parallel benefit system

Analysing large datasets to predict the impact of national benefits policies reveals important insights into how these policies will affect different groups. However, this approach cannot provide a full picture of the situation for low-income households in the UK. This is due to the growing, and increasingly complex, system of locally administered discretionary support schemes that are being used to fill the widening gaps in the mainstream system.

Schemes such as Local Welfare Assistance, Discretionary Housing Payments, the Household Support Fund, Section 13a Council Tax support and the Hardship Fund were intended to address specific crisis situations that could not reasonably be covered by the national benefit system.

A number of temporary discretionary schemes were introduced during the COVID pandemic, such as the COVID Local Support Grant, the £500 Test and Trace Support Payments and packages to help families facing eviction and homelessness. These provided needed support whilst further complicating the social security landscape through which struggling households must navigate.

The growing number of households on benefits in poverty, as well as dwindling council budgets that finance most of these schemes, has meant that, in practice, many schemes are now overstretched.

The localised and discretionary nature of these schemes also creates postcode lotteries for the availability and the level of support, as well as unequal conditions upon which support may be granted. Help generally goes to those who already know about the schemes and can navigate the often complex application processes, rather than those most in need. In addition, less support is available in areas of higher need, as funding for the schemes comes from council budgets.

The same can be said for Council Tax Support, as devolution of working-age support has led to vastly unequal schemes throughout England. An out of work family living in a band D property will pay over £1,300 in council tax next year in the local authority with the least generous scheme, compared to £0 in the local authority with the most generous scheme.

Setting national benefit rates at a minimum level to ensure an acceptable standard of living would free up these local discretionary schemes to serve their intended purpose of addressing specific crises. Alongside this, funding of discretionary schemes and Council Tax Support should be dedicated, linked to need, and contain national guidelines around wide accessibility.

Councils can use data to target discretionary support and maximise the impact of their schemes

In the meantime, councils need to ensure that support is holistic and targeted to those most in need. Policy in Practice’s Low Income Family Tracker (LIFT) platform, which powers the analysis presented here, enables local authorities to target households most affected by increases in the cost of living, and to see how future changes in benefits and costs will impact the financial resilience of their residents.

By analysing their administrative data using LIFT councils are able to maximise the impact of their discretionary schemes at a time of increased funding pressures and to support the most vulnerable families through the cost of living crisis.

Join our free webinar: How 2022 has set up low-income families for 2023

Tuesday 13 December from 11.30 to 12.45. Register here

Join us for our last webinar of 2022 as we review what has been a tumultuous year politically and, more importantly, for households on the lowest incomes. We will review the changes and big issues, from the cost of living and energy crises to the Autumn Statement and the missing million from the labour market.

Through focusing on case studies of different types of households we’ll look at what the changes mean for families now, and what 2023 has in store. Along the way we’ll share the positive impact that organisations we work with are having, and give practical solutions that others can adopt.

Can’t make the date? Register anyway to automatically get the slides and recording.