Universal Credit allows for uprating benefits in-year. The government should take advantage

Alex Clegg Published on 10th November 2022

Reports this week have suggested the government is poised to announce that benefits will rise by September’s CPI figure of 10.1% next April in the forthcoming Autumn statement.

Whilst we and others have argued that uprating benefits by CPI is the bare minimum needed, the government will deserve credit for making the right decision. A real terms benefit cut would have disastrous consequences for families on the lowest incomes during a cost of living crisis.

Uprating benefits is easier with Universal Credit

The minimum expectation should be for benefits to rise by inflation. The government should award free school meals to all households on Universal Credit, and restore work allowances to tackle in-work poverty, improve work incentives and tackle the rising cost of living for families with children.

The government can also move towards a more proactive uprating model that uses the flexibility built into the Universal Credit system to ensure that benefit levels do not lag behind price rises for months.

Universal Credit allows for uprating benefits in-year at short notice, rather than just annually in April, which means that the government’s uprating policy could be much more dynamic in keeping benefits in line with rising prices. The current norm, which sees benefits rise every April by the previous September’s CPI inflation figure, is a relic of the legacy benefits system that required months of lead time to alter benefit levels.

Uprating benefits could be better triggered by CPI figures

Uprating benefits part way through a year could be triggered whenever CPI inflation rises significantly, for example, 4% above the level at the previous uprating. Scheduled uprating every April should also be kept as standard, but should reflect the most recent CPI figure, rather than that of the previous September. This would protect low-income households from sudden cost of living increases that push them into poverty.

If this policy had been introduced in April 2021, for example, it would have triggered uprating in November 2021 and June 2022, on top of annual uprating in April 2022. Benefits would now be 10.6% higher than their April 2021 level. This is because:

- CPI inflation rose by 4% in November 2021 from the April 2021 rate (April 2021 CPI index: 110.1 vs November 2021 CPI index: 114.5), triggering a 4% rise in benefits

- Annual uprating in April 2022 would then have seen benefits rise by a further 2.3%, based on the CPI figure for March 2022 (CPI index 117.1), before another uprating in June 2022 (CPI index 121.8) triggered by a further 4% rise in inflation from March

- The total increase from April 2021 to June 2022 would be 10.6%

The uprating benefits policy is playing catch up with prices

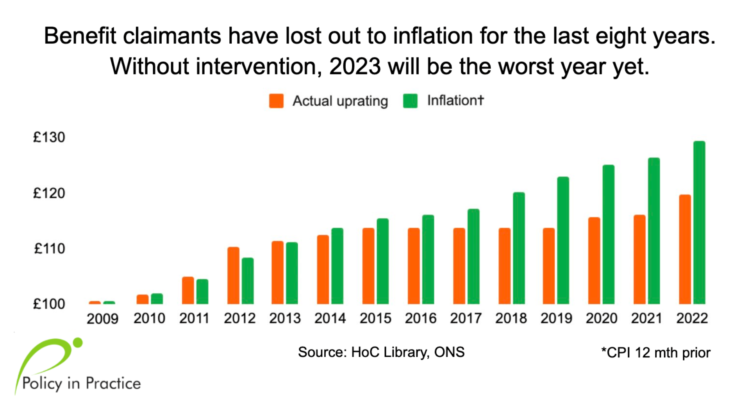

Uprating benefits in April by the CPI figure from the previous September means that the real terms value of benefits always lags six months behind price rises. In 2022 this effect has been exacerbated by two related factors: rapidly rising inflation in general and huge increases in the cost of energy and food in particular. Benefit levels were increased by 3.1% in April 2022, far short of that month’s CPI figure of 9%.

Additionally, low-income households spend a disproportionate amount of their income on fuel and food, meaning they are likely to have experienced increases in their overall budgets that outstrip the official CPI rate. This came at a time when benefit levels have fallen 7.5% lower than their real value in 2009 which highlights how the current uprating policy ensures that benefit rates can only play catch-up with prices at best and cannot restore losses from previous cuts.

Uprating policy should be linked to a minimum standard of living

It also shows how debates around uprating benefits can mask how social security in the UK is not tied to any calculation of how much it costs a household to have an acceptable standard of living.

Starting a new, proactive uprating model from a base level that does this, such as the JRF’s Minimum Income Standard, would provide an adequate safety net that does not allow low-income households to fall into poverty and destitution. It would also implement a clean break from the lasting effects of a decade of benefit cuts and austerity measures.

Universal Credit can deliver a proactive uprating policy that is much needed

The current debate over next year’s uprating is limited to whether or not benefits should be maintained at a level that has declined in real terms for a decade and is not sufficient for a decent standard of living.

Bringing in the proactive, in-year uprating model described above would enable poverty campaigners and organisations to shift the focus of the debate back to setting benefits at levels that are livable for low-income households. It would also realise the potential flexibility that is inherent in the Universal Credit system and move past a flawed and outdated uprating policy.