Help for homeowners: Support for Mortgage Interest and other options

Rory Ewan Published on 02nd August 2023

- In November 2022 only around 1.1% of households on Universal Credit who had purchased a property with a mortgage received Support for Mortgage Interest (SMI) payments

- Designed to support low income households with mortgages in financial difficulty, the low take up shows how SMI is failing to reach households most in need

- Recent changes to SMI eligibility criteria for UC claimants mean many more low income households with a mortgage can access mortgage support if needed

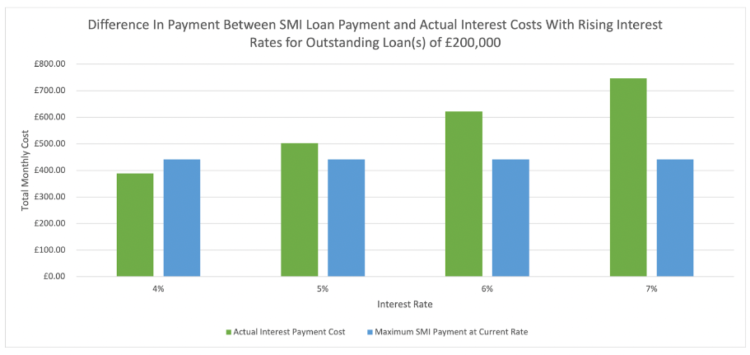

- Whilst welcome, SMI payments are likely to be much less than the actual amount of interest charged if the claimant is on a variable or tracker mortgage rate. The average mortgage interest rate is currently over 6%, with the current SMI rate being 2.65%

- As well as claiming SMI, homeowners who are struggling with rising mortgage costs ask their lenders for forbearance. They can also check if they’re getting all benefits they’re eligible for to make it easier to manage mortgage payments, given that £19 billion of support is unclaimed each year

- With ever increasing interest rates, it is vital that those advising and supporting low income households are aware of the changes in eligibility criteria and the availability of mortgage support

Rising interest rates mean more homeowners face financial crisis

Rising interest rates mean that more low income and middle income homeowners are at risk of becoming unable to afford their mortgage payments.

At the same time, one element of government support for homeowners, Support for Mortgage Interest (SMI), has very low take up.

- In November 2022 only 12,114 claimants were receiving SMI payments. This reflects the previously restrictive eligibility criteria as well as low awareness of the scheme

- Government statistics for 2021 – 2022 show that 230,515 households receiving Universal Credit had a mortgage. The impact of higher interest rates is therefore likely to be widespread. The recent change to eligibility criteria means that the majority of UC households with a mortgage can now access support if needed

- The number of households that face difficulty making mortgage repayments is likely to grow. ONS statistics show that over 1.4 million households in the UK face the prospect of interest rate rises when they renew their fixed rate mortgages in 2023

Without support for mortgage repayments households in receipt of benefits are using savings or credit to meet mortgage costs. Bank of England statistics show that families are increasingly relying on borrowing to cover higher household costs.

For both the mortgage holder and councils it is usually preferable for UC claimants to remain in their home. The private and socially rented housing sectors are already overloaded with a greater demand than supply and councils are struggling with provision and costs of temporary accommodation. Additional repossessions or selling of properties risk increasing these pressures.

The current low take up of SMI suggests that much needed support is not reaching homeowners on low and middle incomes who are facing a financial crisis.

Low take up of Support for Mortgage Interest

The main housing support scheme for homeowners is the Support for Mortgage Interest (SMI) scheme. This is a loan made by the government to households on means-tested benefits to help cover the interest on their mortgage payments. Recent changes to policy mean that the loan is now accessible to more low income households.

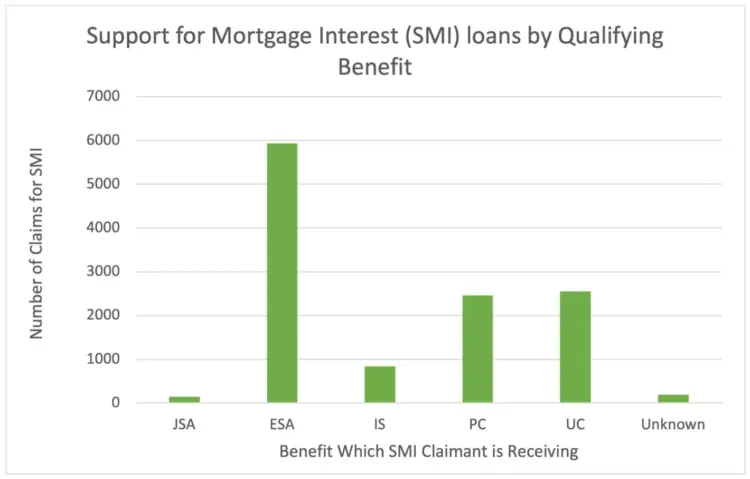

Take up of this support is low with around 98% of eligible households claiming Universal Credit missing out. The most common benefit amongst households that accessed a SMI loan was ESA, which accounted for almost half of all current recipients at 49%. Universal Credit and Pension Credit made up 21% and 20% of recipients respectively.

Rule changes mean up to 200,000 UC households are now eligible for Support for Mortgage Interest

Recent changes to the eligibility criteria for accessing an SMI loan mean that up to an additional 200,000 Universal Credit claimants are now eligible for this support. The change allows households in receipt of Universal Credit to access SMI after three months rather than nine months and is now available to households in work.

The recent change to UC eligibility criteria will enable the majority of UC claimants with a mortgage to access support if needed.

To be eligible for SMI households need to meet one of the following criteria:

- Be in receipt of Universal Credit for three months (three assessment periods)

- Be in receipt of legacy benefits such as Jobseekers Allowance (JSA), Employment and Support Allowance (ESA), or Income Support for 39 weeks

- Be in receipt of Pension Credit

Once approved, eligible households receive a loan that pays a set interest rate on mortgages of up to £200,000 for working-age households, and £100,000 for Pension Credit claimants.

SMI payments are complex and slow to adjust to financial turmoil

SMI interest rate payments are complex to calculate. They are based on the amount of eligible loans and mortgage a claimant has, and what the current standard rate for SMI is.

- Working age claimants can receive support on up to £200,000 of a mortgage and eligible loans. This is £100,000 for people receiving Pension Credit. If a household has a mortgage or loans more than this then this maximum figure of £200,000 or £100,000 is used instead

- The standard rate used to determine mortgage support is based on the average mortgage rate published by the Bank of England. This is adjusted whenever a new rate is introduced when it differs from the current rate by 0.5% or more. The rate is currently 2.65% following a change in May. This means that SMI is likely to be substantially less than the actual amount of mortgage interest payable, given that the average mortgage rate currently over 6%

The SMI rate is slow to adapt to mortgage rate changes and, as variable mortgage rates increase, the gap between SMI support and actual mortgage payments also increases. This will inevitably affect more people as fixed rate mortgage deals end and more households move to variable rate mortgages.

Based on the latest statistics from 2021 to 2022, just over 60% of Universal Credit claimants with a mortgage on their property currently have a mortgage below £100,000. However, over 17,000 claimants currently have a mortgage of £200,000 or more outstanding on their mortgage.

The graph below illustrates the gap between SMI mortgage repayments and actual mortgage interest charged for various mortgage rates for a total loan of £200,000.

Households in receipt of ESA have proportionally taken up Support for Mortgage Interest loans at a greater rate than households in receipt of other benefits. These households often have significant barriers to work and the ability to increase household income. The mechanism for changing the SMI support rate can leave these households vulnerable to wider financial circumstances and a benefits system that can be slow to adjust to changing financial needs.

Loan repayments may cause households to lose increasing equity in their property

SMI support is through a loan that must be paid back to the government with interest.

Repayments on the Support for Mortgage Interest loan have a separate interest rate which is connected to the rate of interest on government loan bonds, currently 3.03%. This interest is accrued daily and added to the existing amount owed each month. The loan becomes repayable when the property is either sold or the ownership transferred.

Because an SMI loan includes interest the amount that is owed for the SMI will increase over time. This means that, over time, borrowers will see the equity in their houses reduce. SMI loans are therefore not the best option for some households and financial advice should be taken to determine if it is the best option for you.

Other support is available to homeowners

Despite its flaws SMI does provide some mortgage support for low income homeowners.

In addition, a recent call to action aimed at mortgage lenders from Chancellor Jeremy Hunt should lead to financial institutions being more receptive to discussions around mortgage options. Specific measures include agreement that homeowners can change to interest-only mortgages, or have an extension of their mortgage for six months without any risk to their credit score, and will be able to go back to their original mortgage deal once their situation improves.

In practice householders requiring support with mortgage payments often take out an SMI loan to partially cover interest repayments before then discussing options for covering the gap in payments with their lender.

Check eligibility for wider support

Over £19 billion of benefits and support goes unclaimed each year. Homeowners may be eligible for other benefit support and should check their entitlement using a reputable, government approved benefits calculator such as Policy in Practice’s free Better Off Calculator. The calculator will also check to see if homeowners and tenants are eligible for social tariffs or reduced utility costs which can reduce outgoings.

Our recent analysis showed that even families with incomes over £60,000 may be eligible for support.

We are working with a number of financial institutions to analyse their customer base and identify who is eligible yet missing out on support. We have found that over a fifth of the customer base is missing out on an average of £200 a month of additional household income.

Financial institutions such as banks and lenders who wish to support households in difficult financial circumstances should contact us to discuss how we can proactively identify and support their customers.