Autumn Statement 2023: Will increases to the Local Housing Allowance reduce homelessness?

Tylor-Maria Johnson Published on 01st December 2023

One of the most anticipated announcements of the 2023 Autumn Statement was the restoration of Local Housing Allowance (LHA) rates to the 30th percentile of local rents, and as part of our Autumn Statement 2023 series, this blog takes a closer look at the impact of the LHA uplift on a privately renting household’s ability to meet their rents.

There are almost 1.7 million privately renting households in England that receive housing support from Universal Credit or Housing Benefit. The OBR forecasts that unfreezing Local Housing Allowance will inject an additional £1.7 billion into housing support over the next five years.

The move to unfreeze LHA rates follows pressure from local government and campaign groups such as Shelter to address the rise in homelessness and temporary accommodation threatening local authority budgets, placing some councils at risk of effective bankruptcy.

With over 100,000 households living in temporary and emergency accommodation, the highest numbers on record, will higher LHA rates be the silver bullet to a multifaceted problem?

New analysis by Policy in Practice shows the Local Housing Allownce uplift will:

- Bring an additional £24 per week into the average household privately renting across England

- Bring 89,100 households receiving housing support out of a LHA rent shortfall, reduce the number of benefit households in private rented accommodation that come up short for rent by 9%

- Be worth the most for households in London and larger properties, but will not reduce the number facing LHA shortfalls because of higher rents and lack of affordable housing

- Benefit households living in smaller properties and households without children

- Benefit over 850,000 Universal Credit households and 140,400 Housing Benefit households subject to the LHA cap will benefit from the increase to the LHA

- Previous Policy in Practice analysis found that for every 1,000 households facing an LHA shortfall, 44 fall into temporary accommodation. The LHA uplift would keep 3,920 from falling into temporary accommodation, saving councils £62.7 million per year in temporary accommodation costs.

What is the Local Housing Allowance?

Introduced in 2008, the Local Housing Allowance (LHA) is the limit set for the housing support a household in private rented accommodation can get from Universal Credit or Housing Benefit.

Over the past decade, freezes to the LHA have divorced it from the actual costs of housing. In 2013, the LHA rate was reduced from the 50th to the 30th percentile of local rents within a defined local area known as the broad rental market area or BRMA.

BRMAs are different from local authority areas. They are often made up of different rental prices because they can contain both wealthy and less wealthy regions. At times, those relying on benefits can still be priced out of areas based on the wider makeup of the BRMA.

LHA rates were then frozen at their 2016 levels until 2020, and then frozen again at their 2020 levels until April 2024. As a result, it has become increasingly common for the housing support determined by the LHA to be less than a household’s rent. This is called an LHA shortfall.

The DWP’s own statistics show that over 850,000 privately renting households on Universal Credit in England faced a shortfall between their rents and the LHA. Of these households:

- 17.3% live in London, and 16% live in the North West; the two regions with the highest rates of LHA shortfall

- 5.8% live in the North East where we find the lowest rates of LHA shortfall

Policy in Practice’s own analysis on benefits administration data shows that:

- 33% of private renters on means-tested housing support face an LHA shortfall

- The average weekly shortfall is £14.00. The highest weekly shortfall is £25.41, and the lowest is £3.40

New analysis: Local Housing Allowance uplift will increase households’ ability to afford rents on means tested housing support

Policy in Practice conducted two original analyses to see how the LHA uplift will impact a household’s ability to afford their rents on housing support.

The Valuation Office Agency calculates LHA rates based on lettings information collected up to the end of September from the previous year. Letting information for LHA rates for April 2024 were collected in September 2023 for release typically in March or April 2024.

To estimate the 2024 – 2025 Local Housing Allowance in the analysis, we use the Valuation Office Agency’s Shadow List of Rents from 2023 and 2022. As the OBR’s LHA eligible rent growth rate of 0.5% does not cover overall market rent increases, we uprated the 2023 LHA shadow rates by the specific rate of LHA growth between 2023 and 2022 for each English BRMA.

In instances where the LHA decreased between 2022 and 2023 (15% or 23/152 BRMAs), we assume that the LHA would have grown by the regional rate of change for private rents from the ONS Index of Private Housing Rental Prices.

We then modelled the impact of the change to the LHA on benefits administration data in October 2023 from six local authorities spread geographically around the UK, representing over 30,000 private renters. To model LHA uplifts against realistic rent levels, we increased private rents by 6% in line with the latest OBR Economic and fiscal forecast.

Finding 1: Restoring the Local Housing Allowance rate to 2023 levels will result in an additional £24 per week in housing support

Policy in Practice’s new analysis shows that restoring the LHA rate is a welcome boost to housing support for households on means-tested benefits.

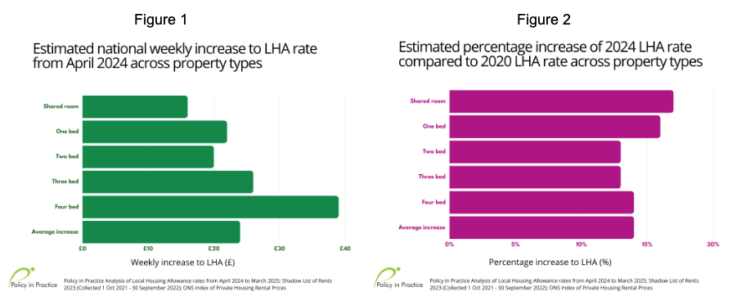

Figure 1 shows that on average the restoration of the LHA to 2023 local rents will result in an additional £24 per week from £164.69 to £189.16 per week in housing support for means-tested benefits. This works out to an average 14% increase in the 2024 LHA compared to the 2020 LHA.

When considering the £ amounts, households in larger accommodation will see larger increases on average. For instance, households in a four bedroom property can see an average increase of £39 per week, compared to those in shared accommodation seeing an average increase of £16 per week.

However, households in smaller properties tend to have a higher percentage growth in the LHA compared to 2020. Figure 2 shows that a shared room and one bedroom properties see the highest boost. For a shared room the LHA goes from £79.96 to £95.52 per week, which is an increase of 17%, whilst a one bed increases from £130.48 to £152.40 per week, which is a 16% increase.

Since the shared accommodation rate is the maximum amount that a single person under 35 can receive, the LHA uplift has a generational impact in the level of support a household can receive.

Finding 2: Local Housing Allowance uplift will reduce the number of households facing Local Housing Allowance shortfall by 9%

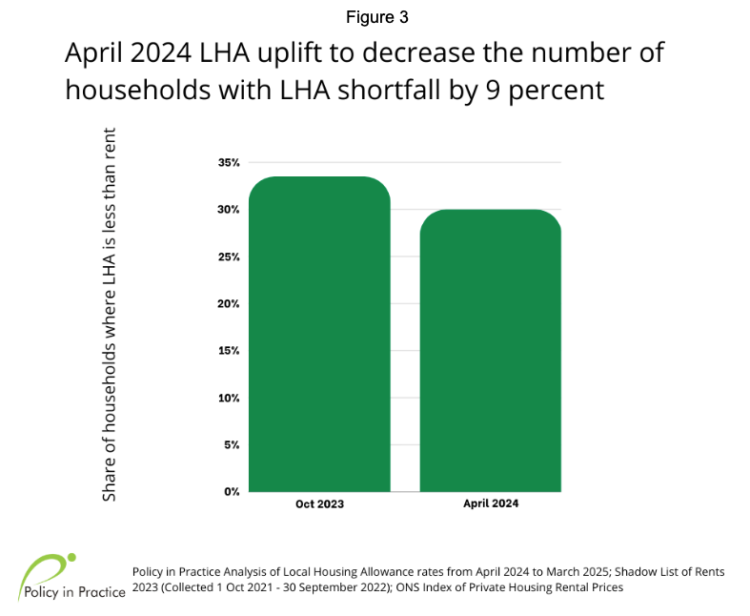

Over 26% of households in the administrative data we used for this analysis are private tenants. This data shows that in October 2023, one in three private tenants had an LHA shortfall. These households faced an average weekly LHA shortfall of £14, or £60.83 per month.

Figure 3 shows that, as a result of the LHA uplift in April 2024, there will be a 9% or a 3 percentage point reduction in the number of households with an LHA shortfall.

For the households that continue to be impacted by the LHA, the average amount of the LHA shortfall will also fall by £1.50 from £14.00 to £12.50 per week, or £54.31 per month.

Finding 3: The Local Housing Allowance uplift will have little impact on rates of Local Housing Allowance shortfall in London despite sizeable boost to Local Housing Allowance rates

When London local authorities are excluded from the analysis the LHA uplift has a larger impact. For private renters outside London, we estimate there will be a 19% or a 5.6 percentage point reduction in the number of households with an LHA shortfall, falling from 34.8% to 29.1% of households.

Households that continue to be impacted by the LHA outside of London will see their weekly LHA shortfall decrease by £1.77 from £11.30 to £9.53, or £41.40 a month.

For private renters in the two London councils within this analysis the LHA uplift makes no real difference in the rate of those impacted by the LHA cap.

We estimate that 31% of private renters receiving housing support will continue to owe rents that are higher than the LHA. While this may not be the case for all London councils, and wider analysis is required, neither of the data sets used were at the margins for London.

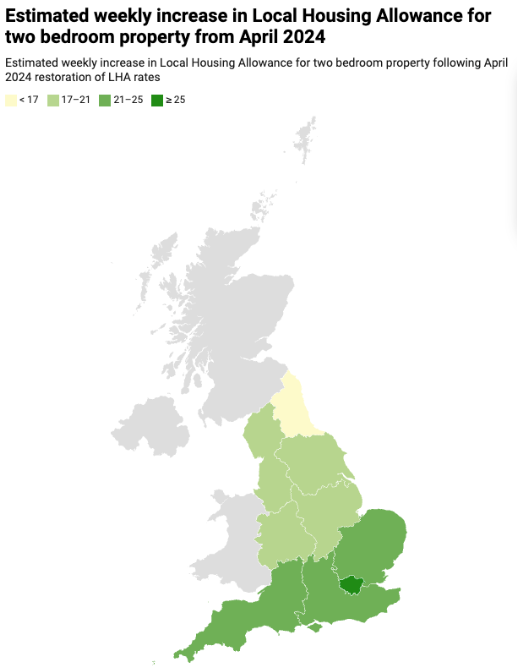

Figure 4 shows the estimated weekly increase in the LHA for a two bedroom property across regions in England.

A household living in a two bedroom property in London will receive an additional £25 per week in housing support per week whereas a household living in the North East will only see a £8 weekly uplift to their LHA amount.

However, higher rents in London minimise the impact of the LHA increase for London broad rental market areas.

Even though households will receive more housing support, higher rents and lack of affordable housing mean households will still continue to face LHA shortfalls.

London Councils showed that 1 in 50 Londoners are homeless and living in temporary accommodation. Many London households will continue to be at risk of needing temporary accommodation because they cannot find affordable housing.

Finding 3: Households living in smaller properties are better off

Our analysis finds households living in one bedroom properties will get the largest boost to their housing support because of the LHA uplift.

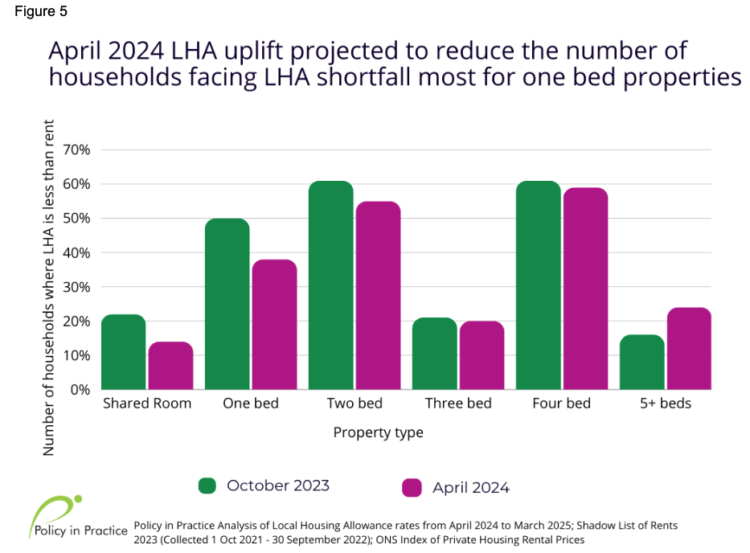

Figure 5 shows the share of households with an LHA shortfall by property type. Using administrative data from Oct 2023, we found households living in one, two, and four bedroom properties had the highest rates of facing an LHA shortfall.

As a result of the LHA uplift, there will be a 38.1% reduction in LHA shortfall rates for households living in shared rooms, falling from 21.8% to 13.5%. This is the largest percentage decrease in LHA shortfall rates of any property type.

One bedroom properties will see a 23.8 % reduction in their LHA shortfall rates, falling from 50% to 38%, whereas the number of households occupying larger properties with five or more bedrooms facing a rent shortfall will increase by 44% from 16.5% to 23.7%.

Finding 4: More households living in larger properties will face a Local Housing Allowance shortfall

Figure 2 also shows that larger properties will continue to face LHA shortfalls at high rates. Households living in three and four bedroom properties will see marginal decreases in the number of those facing LHA shortfalls.

This is interesting because those living in larger properties are estimated to receive a larger increase to their LHA.

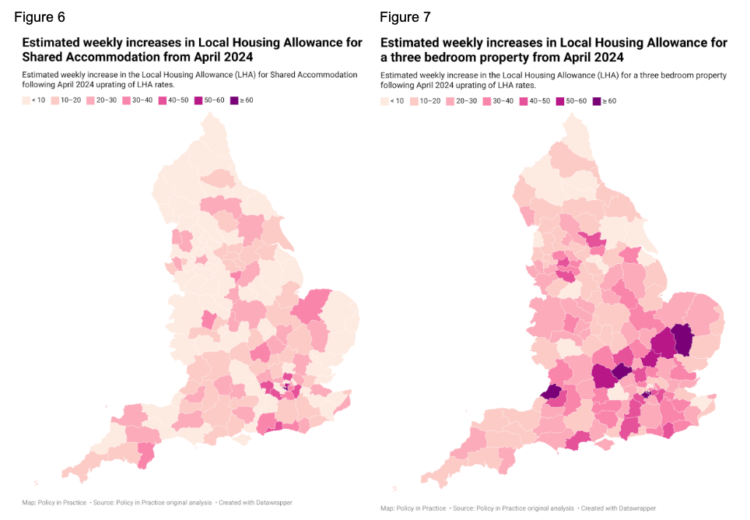

Figures 6 and 7 show that LHA weekly increases across all English broad rental market areas. The amount of the LHA weekly increase will vary across broad rental market areas with some clear regional variations.

The map on the left shows the estimated weekly increase in LHA for shared accommodation, whilst the map on the right shows the weekly increase for a two bedroom property.

Most shared accommodation will see an additional £16 per week which is a 17% weekly increase in the LHA. Whereas, most three bedroom properties will see an additional £26 per week which is a 13% weekly increase in the LHA.

Both are sizable increases to LHA rates for both property types. However, smaller properties have a slight advantage seeing a larger overall percentage increase to their LHAs.

The slight to no reduction in the LHA shortfall rate for larger properties likely reflects the increasingly high prices of rents on larger properties. Despite the significant increase in LHA rates for those in larger properties, projected rents will continue to rise and at times outpace LHA-based housing support.

Our analysis shows that households living in properties with five or more bedrooms are more likely to be at risk of facing an LHA shortfall. This is likely to impact larger families, ethnic or multi-generational households more. In instances when large families cannot afford the right sized home, they may rent homes with too few bedrooms, leading to poor health outcomes.

This is in part due to housing support policy. Properties with five bedrooms or more will receive housing support based on the LHA for a four bedroom property.

Despite the LHA rate for four bedroom properties going up, five bedroom properties rents will continue to outpace any increase in the four bed LHA rate.

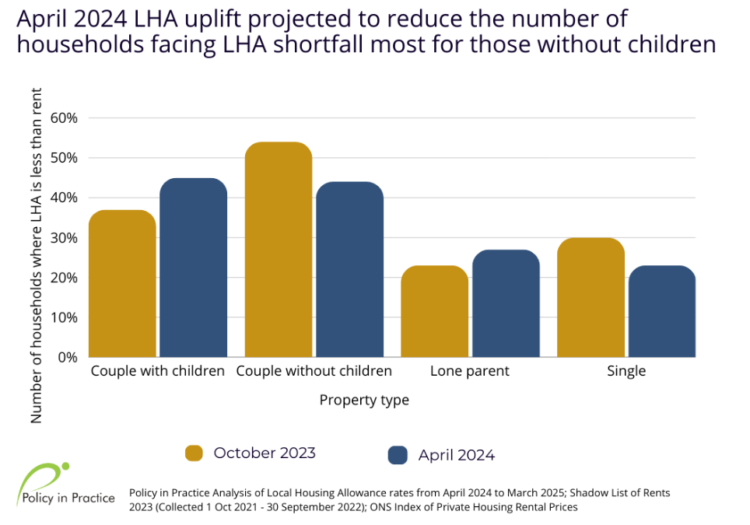

Finding 5: Local Housing Allowance uplift is worth more for households without children

We estimate that the LHA uplift will help couples without children and single parents most in meeting their rents.

Figure 8 shows that the rate that couples without children face an LHA shortfall decreases by 10 percentage points, and single person households have their LHA shortfall rates drop by 8 percentage points.

Couples with children and lone parents are more likely to face an LHA shortfall than their counterparts without children after the LHA uplift.

Families with children need larger homes and may be eligible for LHA rates based on more than one bedroom as a result. However, as rents for larger properties are often higher than rents for a one bedroom accommodation, larger households have a harder time finding accommodation within their local LHA.

Additionally, households with children are most likely to be benefit capped.

The DWP’s latest statistics for 2023 show that 3,351 households on Housing Benefit and 79,102 households on Universal Credit are affected by the benefit cap.

- Nine out of ten benefit capped families had children

- Five out of ten benefit capped families had a child under five

- Two out of three benefit capped families were single parents

- One out of three benefit capped families were single parents with a child under five

When a household’s benefit income exceeds the benefit cap, their housing support will be reduced accordingly.

Since the benefit cap is frozen, many households may still find themselves dipping into their standard allowance to make ends meet.

The restoration of the Local Housing Allowance saves councils over £62.7million a year on temporary accommodation costs

Our previous analysis shows that LHA shortfalls are proven to drive homelessness. For every 1,000 households experiencing an LHA shortfall, 44 would need temporary accommodation.

The Chancellor’s announcement in the Autumn Statement 2023 goes some way towards reducing the number of people experiencing an LHA shortfall and therefore at risk of falling into temporary accommodation.

This analysis finds that the LHA uplift would reduce the number of privately renting households facing an LHA shortfall by 9%. Across English, this would mean 89,100 fewer households on housing support will be impacted by the LHA shortfall, keeping 3,920 from falling into TA.

In 2023 English councils paid more than £1.7 billion for 104,000 households in temporary accommodation, working out to about £16,000 per every one household in temporary accommodation.

If the LHA uplift keeps 3,920 households from an LHA shortfall, then it saves councils over £62.7 million a year in temporary accommodation costs.

Council spending on Discretionary Housing Payments (DHPs) is likely to become more flexible. One of the main aims of DHPs is to reduce the shortfall between a household’s housing support and their actual housing costs.

DHP funding is not linked to shortfall rates or housing costs in an area. Some councils may overspend their DHP budgets to address welfare reforms like the LHA shortfall, and have less to spend on other purposes.

Reduction in rent arrears and temporary accomodation numbers frees up council DHP budgets and can, in turn, allow for more targeted support to be given to those most in need.

Persistently high levels Local Housing Allowance shortfall will continue to drive homelessness

This analysis should also make us concerned. Even with the uplift, 30% of those privately renting will still not be able to afford their rents at the LHA rates available to them, especially in London, and for larger households.

Although the re-pegging of the LHA is welcome, it is a relatively small drop in the ocean towards fixing housing policy and the structural issues of the current housing market.

It is worrying that the LHA rate is currently planned to be frozen for the following year. Short term savings from freezing the LHA cause larger long term costs to households and to the council.

Instead, the LHA rate ought to be uprated yearly to keep in synchronisation with local rents.

Similarly, in times of housing crisis and fast rising rents, the process for determining LHA rates might be moved from September of the previous calendar year, to a time closer to April, to keep up with fast changing rental increases.

Increasing the LHA does not make more housing available, nor does it address the lack of affordable housing, meaning costs could still increase beyond what low income households can afford.

It also does not fully relieve the pressure councils face to help households meet their rents.

Structural change, building more homes, particularly at social rents, and allocating more funding to councils to meet the needs of their residents, are needed to tackle the continued housing crisis.

Next steps

- Read Autumn Statement 2023: A step forward after many steps back

- Read Autumn Statement 2023: Uprating benefits – the long view

- Read Autumn Statement 2023: Support versus sanctions – how can we best help people into work?

- Join our free webinar Policy review of 2023 and what 2024 may hold on Wednesday 6 December. Register here